Build vs. Buy Payment Infrastructure

Feature Comparison

| Capability | Build In-House | Modern Treasury |

|---|---|---|

| Time to production | 6-18 months. Each rail is a separate build. | Days to weeks. One API across all rails. |

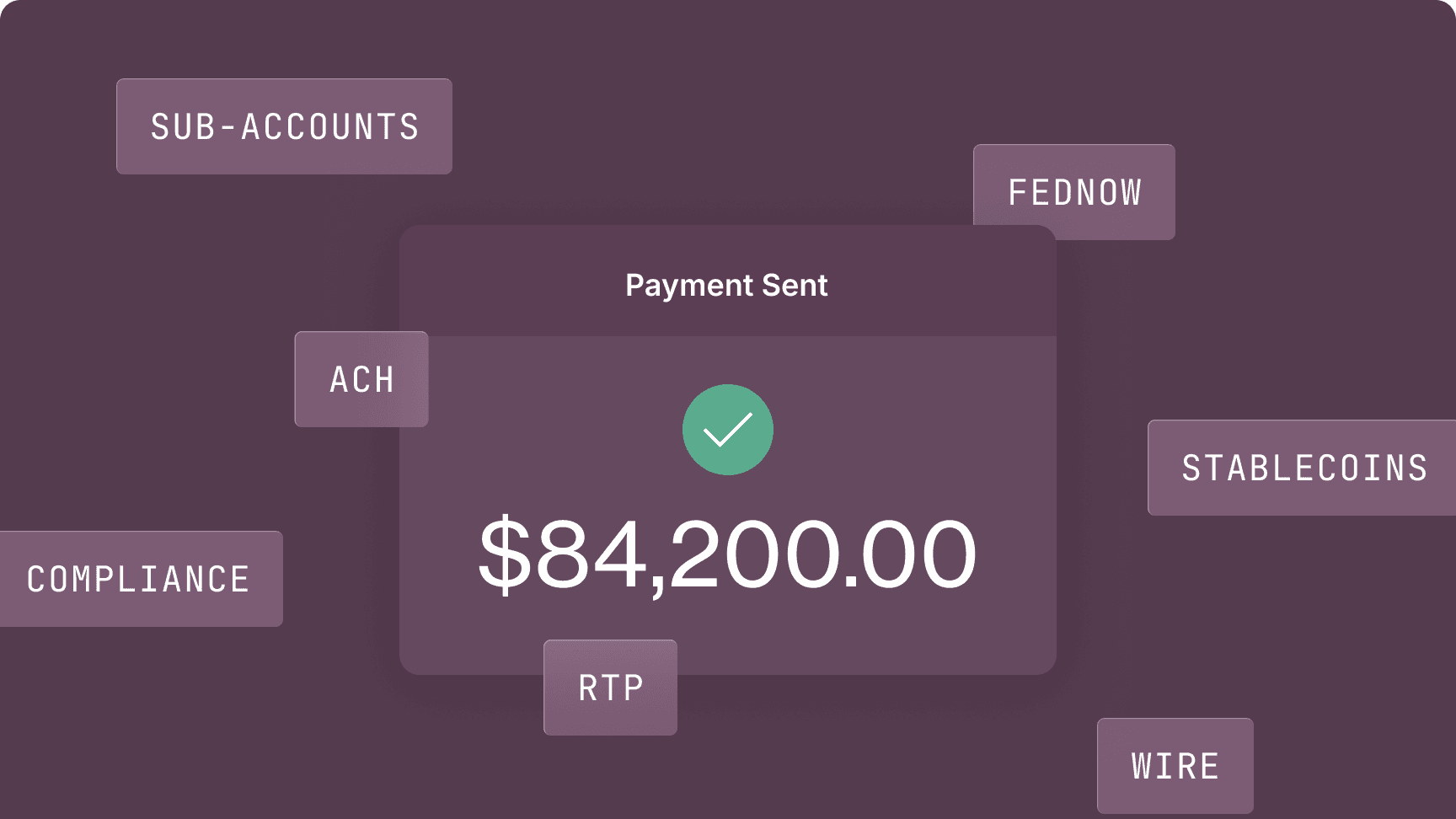

| Payment rails | Each rail requires its own integration, file formats, and error handling. | ACH, RTP, FedNow, wire, checks, and stablecoins (USDC) through a single API. |

| Ledger | You're responsible for accuracy and auditability. | Ledger-backed and audit-ready. $600B+ in payments processed. |

| Reconciliation | Manual or custom-built. Breaks at scale. | Automated across banks, rails, and internal accounts. |

| Compliance (KYC/KYB/AML) | You build and maintain your own programs, vendors, and monitoring. | Built-in, or bring your own program. |

| Sub-accounts | Custom database modeling. You build and maintain the data model. | Programmable sub-accounts for funds, balances, and flows across entities. |

| Bank relationships | You open and manage each bank relationship individually. | Use our bank partners, or bring your own bank. |

| Adding new rails | Each new rail is a near-complete rebuild and net-new compliance approval process. | New rails through the same API. No architecture changes. |

| Ongoing maintenance | 1-2 FTEs minimum for bank connectivity, compliance updates, and rail changes. Indefinitely. | Handled by Modern Treasury's platform and engineering team. |

Where In-House Builds Hit Their Limits

Adding new rails

Adding RTP, FedNow, or stablecoins often takes as long as the first integration. Most in-house architectures assume a single rail and require significant rework for additional settlement mechanics.

Reconciliation at scale

Manual reconciliation breaks down as transaction volume grows. At thousands of transactions per day, unreconciled items accumulate, investigation time compounds, and financial reporting falls behind.

Compliance scope creep

Compliance requirements expand as you add sub-accounts, new rails, and third-party funds. Each addition requires new vendor integrations, monitoring capabilities, and reporting workflows.

Engineer turnover

Payment infrastructure is specialized. Losing the engineers who built core systems like NACHA file generation or reconciliation logic creates institutional knowledge gaps that are expensive to recover.

Payments Processed

Across Fiat and Stablecoins

Not Months to Go Live

Different Platforms, Different Infrastructure

Building in-house is the right call when:

- Payments are your core product, not a feature of your product

- You have a team of dedicated engineers with a long-term maintenance plan.

- You are a bank or licensed financial institution with existing bank connectivity and compliance

- Your requirements are narrow and unlikely to change: one rail, one bank, one use case.

Modern Treasury is the right call when:

- Payments support your product but are not the product.

- You need ACH, RTP, FedNow, wire, and stablecoins through one API

- You are managing sub-accounts or third-party funds and need a production-grade ledger.

- Go live in days, not months, without bank onboarding

- You'd rather invest engineering time in your core product, not payment infrastructure maintenance.

Common Questions About Building vs. Buying Payment Infrastructure

Six to 18 months with a team of dedicated engineers. The bank integration is the fastest part. Ledgering, reconciliation, and compliance account for most of the timeline.

Modern Treasury's customers usually reach us when they need a second payment rail or when reconciliation and compliance overhead starts consuming engineering time.

Yes. Modern Treasury's Bring Your Own Bank model is designed for this. Start with our bank partners, then add your own bank relationships as you scale. Your integration, ledger, and API contracts stay the same.

Modern Treasury operates as a managed PSP: bank connectivity, compliance, and money movement through a single API. Building in-house means owning each of those systems directly. A managed PSP gives you hosted infrastructure with the option to bring your own bank for full control.

Modern Treasury includes a real-time double-entry ledger that can serve as your system of record. Some teams choose to keep their own ledger. We support both approaches.

If payments are your core product and your competitive advantage depends on owning every layer of the stack, building makes sense. Banks, licensed money transmitters, and companies where the infrastructure itself is the product should evaluate carefully.