Embedded ACH for B2B Platforms: What to Know Before You Build

Feature Comparison

| Capability | Standard ACH Processing | Embedded ACH for Platforms |

|---|---|---|

| Who it’s designed for | A single business moving its own money. | A platform moving money on behalf of many users. |

| Setup time | Weeks. | Months, if building direct bank relationships. |

| Sub-account support | None | Move liquidity globally without parking capital in every market |

| Return handling | Returns hit one account | Required; each user needs separate balance tracking |

| Reconciliation | One ledger. | One ledger per user, reconciled against a master |

| Compliance ownership | Your business | Your business plus every user you originate for |

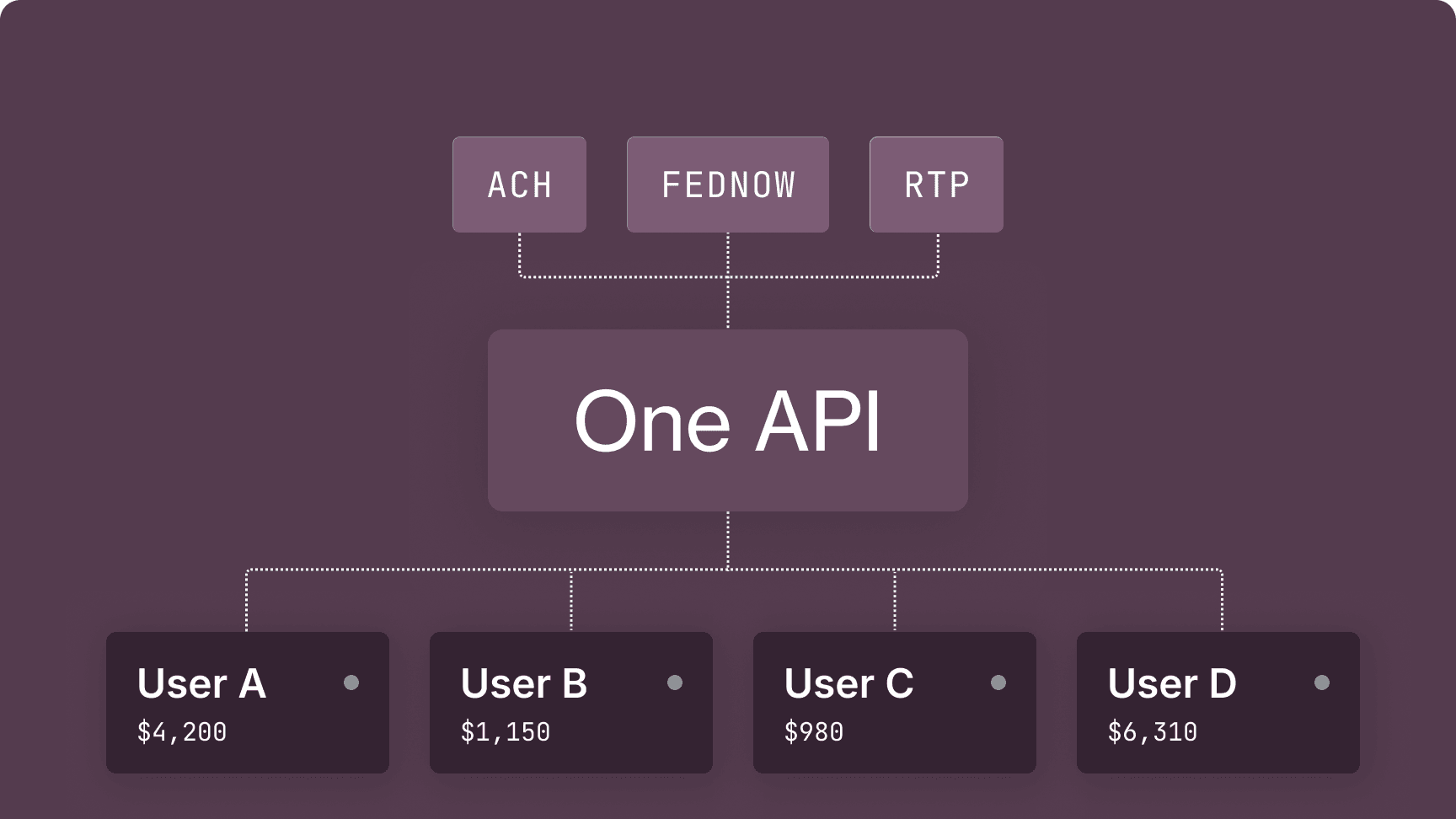

| Multi-rail access | ACH only | ACH, RTP, FedNow, and wire, depending on infrastructure |

| Scale path | Volume-based bank renegotiations | Determined by your infrastructure choice upfront. |

Where Standard ACH Breaks Down for Platforms

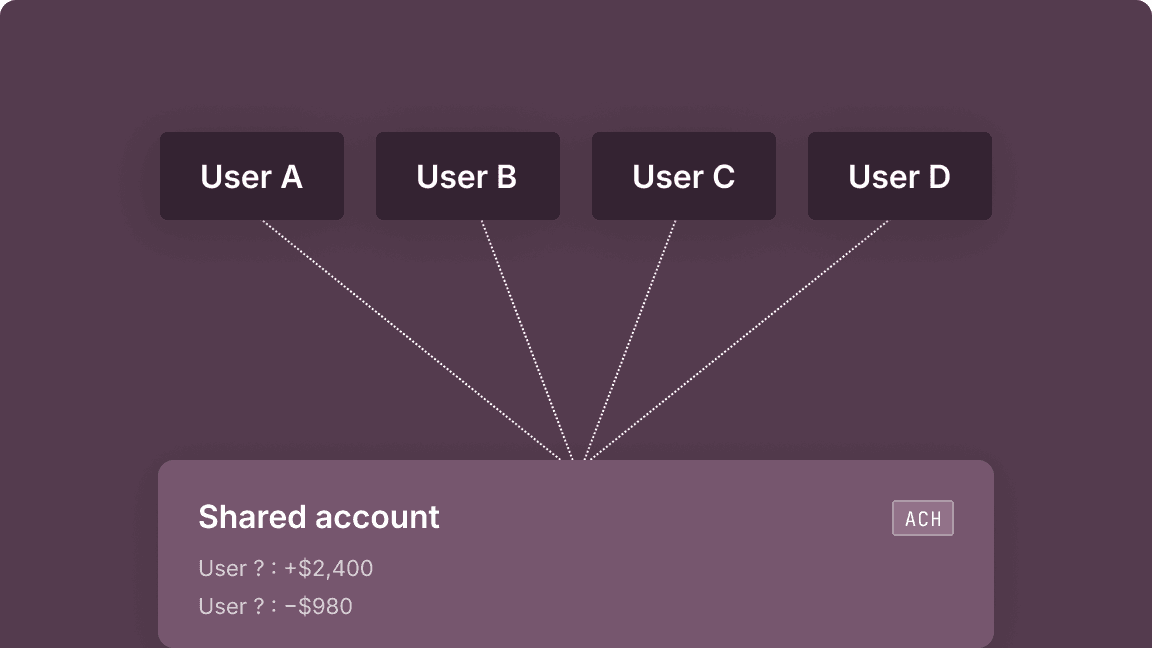

Each user needs their own money movement

A single bank account handles one entity's payments. Platforms with hundreds of users each need their own balances, history, and return exposure — none of which standard bank ACH provides.

Returns don’t route themselves

ACH returns land at the originating account. Your team has to figure out which user each one belongs to, update their balance, and notify them — manually, or with custom tooling your engineers now own indefinitely. At scale, it's a full job.

Compliance applies to every user, not just the platform

When you originate on behalf of users, NACHA's rules apply to every transaction. KYC, KYB, debit authorization, and return-rate thresholds all have to hold at the user level — something most platforms miss until a compliance review.

Bank relationships don’t grow with your product

Direct origination rights take six to twelve months to establish, and the relationship caps what you can offer — volume tiers, renegotiations, and approvals for each new use case. Your product roadmap ends up gated by your bank agreement.

Return rates become your problem at scale

NACHA monitors return rates at the originator level. One user with poor payment hygiene can push your aggregate rate toward a threshold — and on direct bank ACH, that exposure is entirely yours. Purpose-built infrastructure sets limits per user first.

Payments Processed

Across Fiat and Stablecoins

Not Months to Go Live

Different Platforms, Different Infrastructure

Go direct-to-bank when:

- You process high volume for a small number of users.

- You have in-house NACHA compliance expertise.

- You have 12+ months and dedicated engineering bandwidth.

- You don't need per-user balances or real-time rails.

Use Modern Treasury when:

- Your users each need their own payment flows.

- You want to go live in days, not months.

- You can't staff a full bank compliance function.

- You need ACH, RTP, and FedNow through one API.

Common Questions About Embedded ACH for Platforms

Embedded ACH means a software platform offers ACH pay-ins and payouts as a feature within its product, without its users needing their own bank accounts or NACHA originator status. The platform integrates with a payment infrastructure provider that holds the bank relationship, handles ACH origination, and manages compliance on the platform's behalf. Each user gets their own virtual account and transaction history. The platform's users see ACH as a native product feature; the infrastructure sits underneath.

A B2B platform that processes ACH on behalf of its users acts as an intermediary between its users and the banking system. When a user initiates a payment, the platform's infrastructure provider originates the ACH transaction, routes it through the appropriate bank, and settles funds to the correct sub-account. Returns, compliance checks, and balance updates all happen at the sub-account level, not the platform level. The platform sees a unified ledger view across all users.

NACHA governs all ACH origination in the US. For platforms, the key rules cover return rate thresholds, debit authorization requirements, and same-day ACH cutoff windows. NACHA monitors return rates at the originator level, which means a platform originating ACH for hundreds of users needs to manage return exposure across its entire user base, not just per transaction. Platforms also need to ensure users have proper debit authorization on file before initiating ACH pulls. Violating NACHA thresholds can result in probation or loss of origination rights.

ACH credit pushes money from the originator to a receiver, for example a platform paying out to a user's bank account. ACH debit pulls money from a receiver's bank account to the originator, for example collecting a payment from a user. For platforms, both directions have different compliance requirements. ACH debits require an authorization from the account holder before the pull. ACH credits are lower risk but still subject to return codes if the destination account is closed or invalid. Most platforms need both directions as their product matures.

Returns need to route to the correct user account, not the platform's primary account. That requires either custom internal tooling to match returns to sub-accounts, or infrastructure that handles return routing natively. Platforms that underinvest here find out when return rates trigger a NACHA threshold review.

Return rates compound when platforms originate for many users without per-user controls. The most effective approach is setting debit authorization requirements before allowing ACH pulls, using micro-deposit or instant verification before first transactions, and monitoring return codes by user rather than in aggregate. R01 (insufficient funds) and R02 (account closed) are the most common returns and are preventable with pre-transaction account verification. Infrastructure that surfaces return data at the user level lets platforms identify and restrict users with poor payment history before they affect platform-wide return rates.