Modern Treasury vs. Adyen

Feature Comparison

| Capability | Adyen | Modern Treasury |

|---|---|---|

| Primary use case | Global card acquiring and unified commerce — accepting payments across online, in-store, and in-app channels. | Payments infrastructure built for multi-rail money movement where ACH, RTP, FedNow, stablecoins and ledgering are first class. |

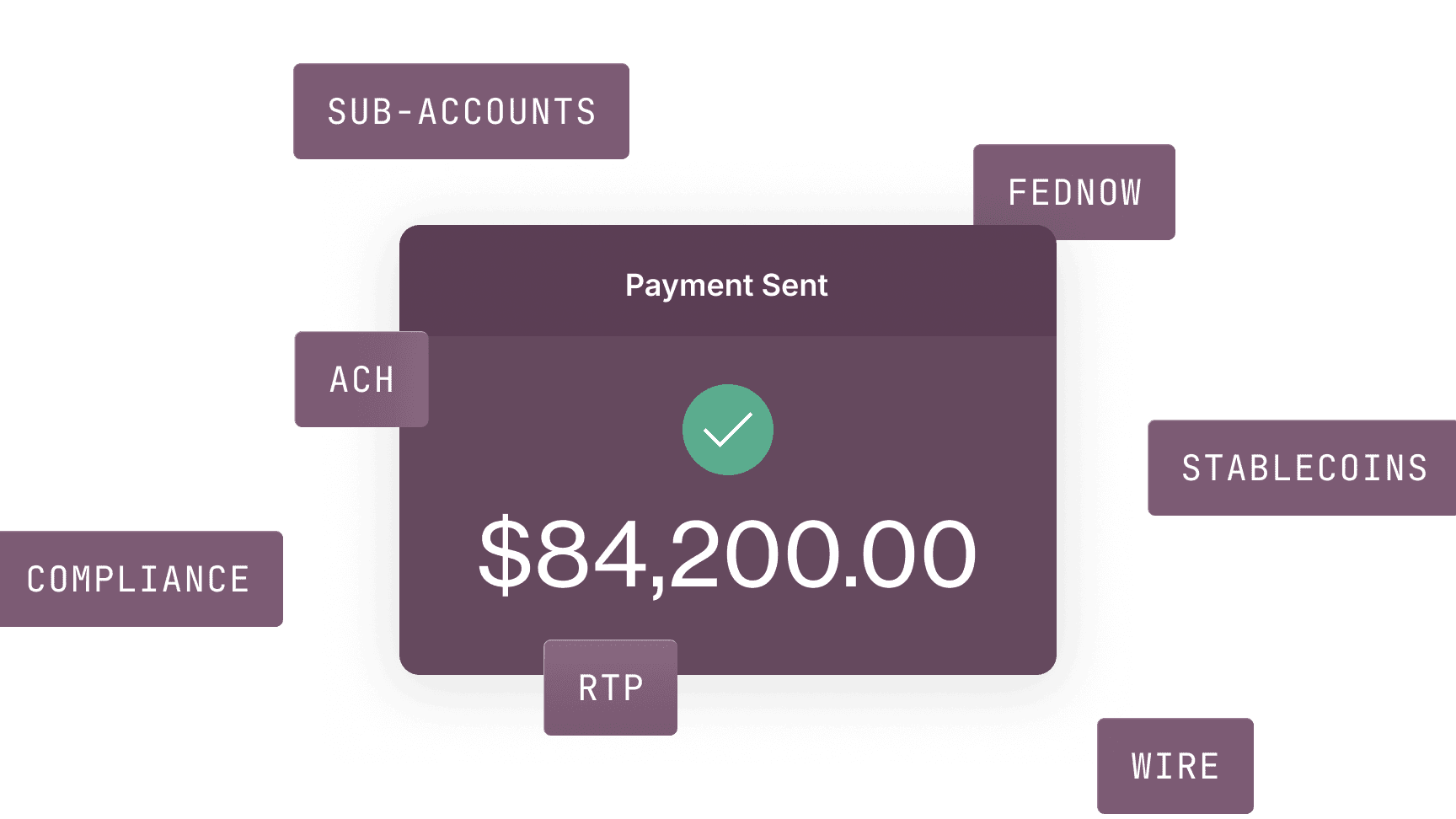

| Payment rails | Card acquiring is the core. Bank rails are available in supported regions, primarily for payouts. | ACH, RTP, FedNow, wire, and stablecoins (USDC) on one API. Card acceptance is not the focus. |

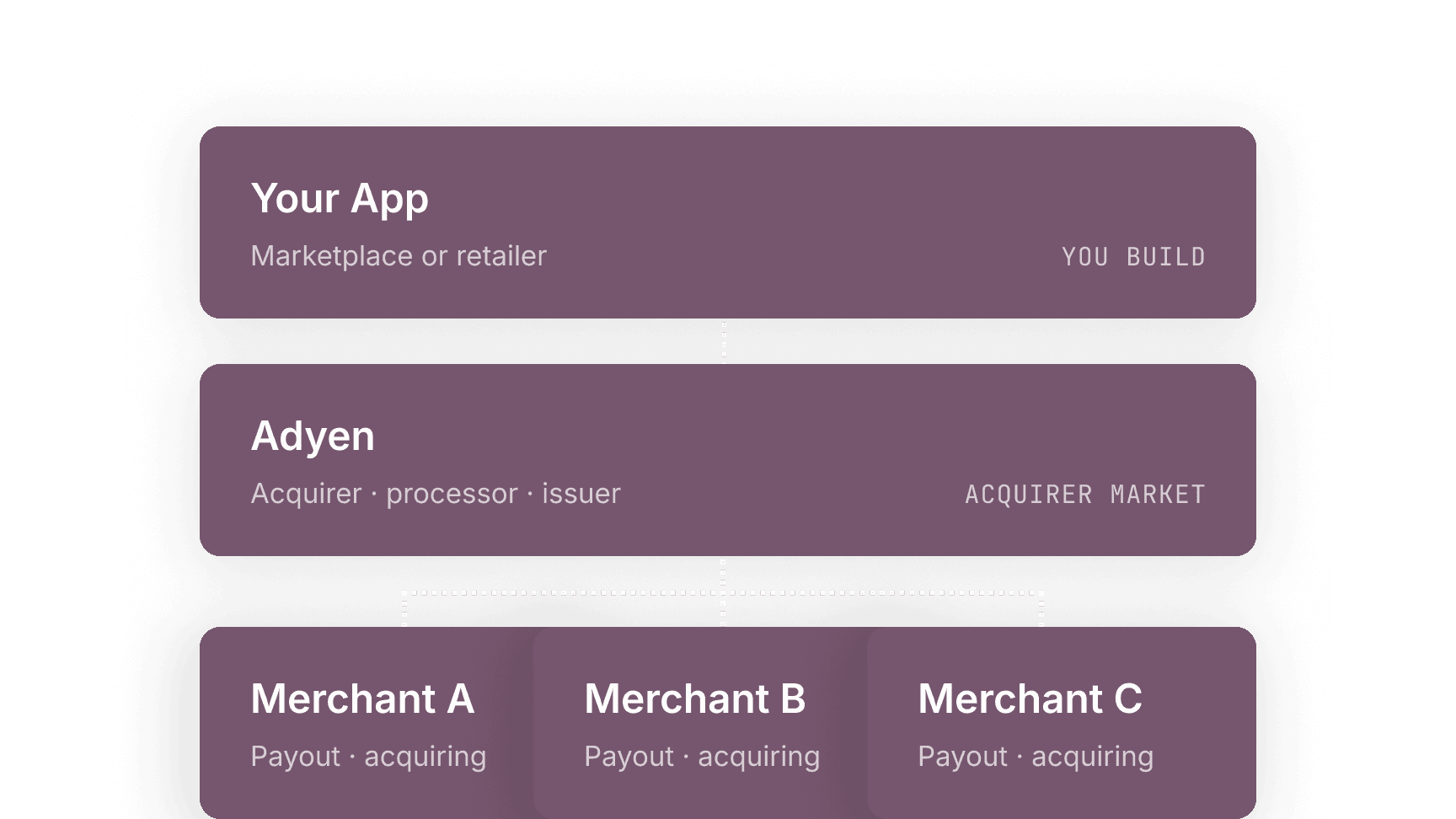

| Geographic coverage | Global. Adyen operates as a licensed acquirer across multiple regions. | Enable users in 90+ countries to receive, hold, and send U.S. dollars through named U.S. accounts. |

| Real-time ledger | Adyen for Platforms exposes balance accounts and transfer instruments for marketplace flows. | A single, immutable system of record to track balances, transactions, and money movement across your entire stack. |

| Programmable sub-accounts | Balance accounts in Adyen for Platforms model marketplace splits and payouts. | Sub-accounts as internal financial primitives — model funds, balances, and flows across entities in your system. |

| KYC / KYB / AML | Compliance is built into Adyen's onboarding flows for sub-merchants and platform users. | Use Modern Treasury's compliance tooling, or bring your own KYC/KYB/AML provider. |

| Stablecoins | Stablecoin rails are not part of the standard product. | Supports USDG, PYUSD, and USDC alongside fiat rails on the same API. |

Where the Approaches Differ

Card-first design

Adyen's core is global card acquiring. Platforms whose primary motion is bank-rail money movement use a different shape of infrastructure.

Rail coverage in the US

RTP and FedNow are not central to Adyen's US offering. Modern Treasury supports them as first-class rails.

Ledger as a product

Modern Treasury offers a dedicated double-entry ledger to track balances, transactions, and money movement across your entire stack.

Stablecoins

Stablecoin rails are not part of the Adyen product. Modern Treasury supports USDC alongside fiat on the same API.

Different Platforms, Different Infrastructure

Adyen is best for:

- Global enterprise card acquiring and unified commerce

- Omnichannel retail and travel

- International marketplaces with sub-merchant onboarding

- Teams that want a single licensed acquirer across regions

Modern Treasury is best for:

- B2B platforms running ACH, RTP, FedNow, and wire at scale

- Vertical SaaS embedding payments into their product

- Platforms managing sub-accounts or third-party funds

- Fintech platforms requiring ledger and compliance infrastructure

- Companies that need one platform for fiat and stablecoins

Payments Processed

Across Fiat and Stablecoins

Not Months to Go Live

Common Questions About Modern Treasury vs. Adyen

Adyen is a global payment processor and licensed card acquirer. Its core is accepting card payments across online, in-store, and in-app channels, with marketplace and platform features layered on top. Modern Treasury is payments infrastructure built for bank-native money movement where ACH, RTP, FedNow, stablecoins and ledgering are first class. The two products solve different parts of the payments stack.

Adyen supports ACH for select payout flows. RTP and FedNow are not central to the US offering. Modern Treasury supports ACH, RTP, FedNow, wire, and stablecoins as first-class rails on a single API.

No. Modern Treasury is not a card acquirer. Many platforms pair Modern Treasury for bank-rail payments and ledger infrastructure with a card acquirer like Adyen for card acceptance.

Yes. Modern Treasury's Global USD Accounts let users in 90+ countries receive, hold, and send U.S. dollars through named U.S. accounts, with international flows also supported through partners and stablecoin rails. Platforms with global card-acquiring needs typically combine Modern Treasury with a global processor.

If your primary motion is global card acquiring, omnichannel retail, or international marketplace card acceptance, Adyen is built for that. If your platform is moving money over bank rails — ACH, RTP, FedNow, wire — or needs a real-time ledger and compliance infrastructure for B2B fund flows, Modern Treasury is purpose-built for that.