Modern Treasury vs. Bridge

Feature Comparison

| Capability | Bridge | Modern Treasury |

|---|---|---|

| Primary use case | Stablecoin-first payments infrastructure: stablecoin orchestration, issuance, on/off-ramps, and global payouts. | Bank-native payment operations for B2B platforms, moving money across ACH, RTP, FedNow, wire, and stablecoins with a real-time ledger. |

| Stablecoin orchestration | A core strength: stablecoin payins, payouts, and on/off-ramps. | Native orchestration on the same API as fiat rails (fiat → stablecoin → fiat), reconciled across both. |

| Stablecoin issuance | Supported: issue and manage your own stablecoin as a core product. | Not a stablecoin issuer. Modern Treasury orchestrates stablecoin movement alongside fiat rails. |

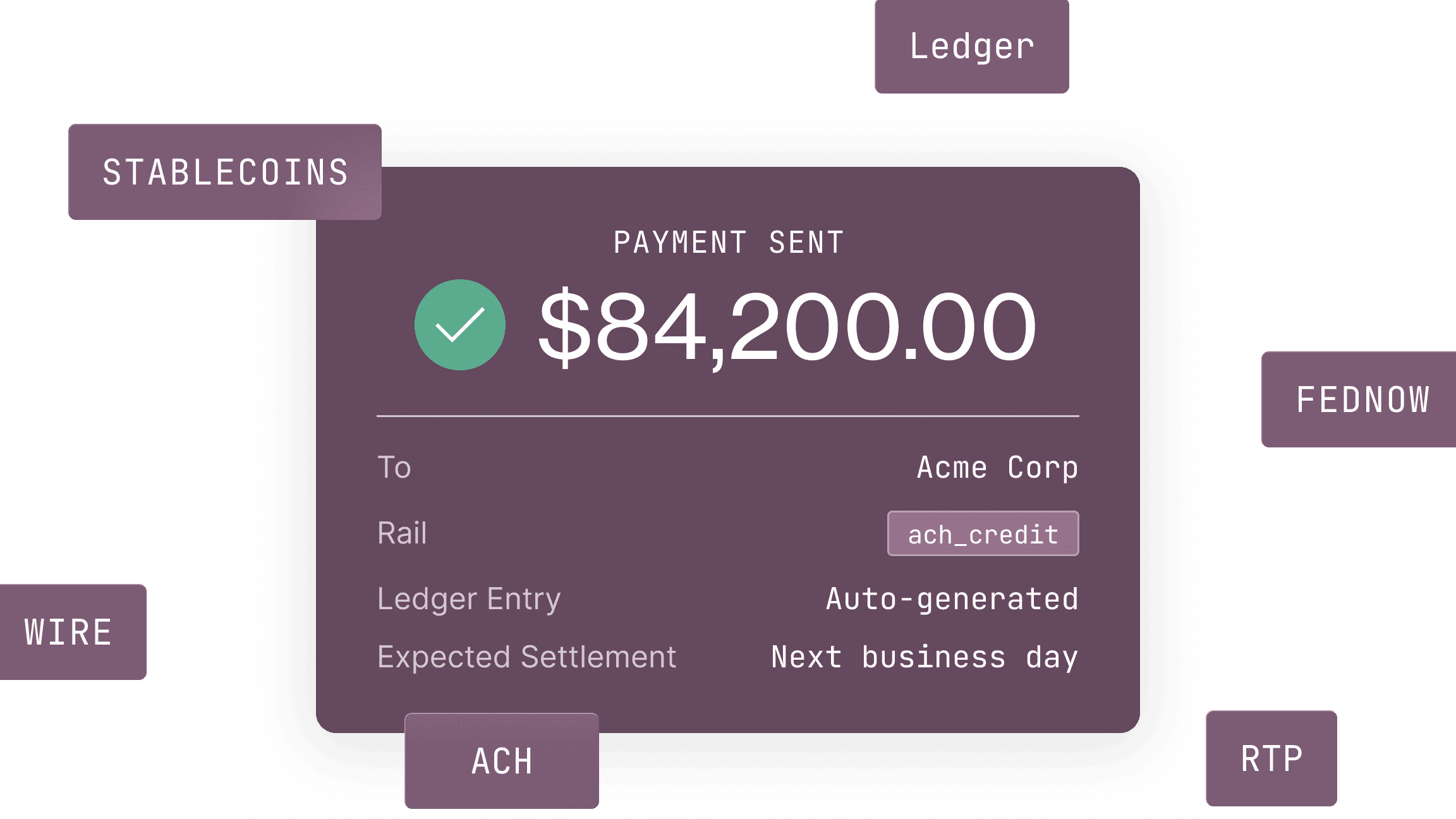

| US fiat rails & ACH pull | ACH and wire supported; ACH is oriented to settlement, and native ACH pull (debit) is not evidenced. | ACH credit and debit, including native ACH pull to collect funds directly from customer bank accounts, plus wire. |

| US instant rails (RTP / FedNow) | FedNow (instant USD) supported; RTP is not. | RTP and FedNow are native, first-class rails for send and receive. |

| Bank connectivity & verification | Not part of the product. | Built-in bank connections and account verification. |

| Named US accounts | Pass-through only: an account/routing number to receive USD and auto-convert to stablecoins. | Full sub-accounts: fully-functional USD Payment Accounts which can be used for fiat-only activity or in conjunction with stablecoin accounts. |

| Local / international rails | Supports local rails across Europe, Mexico, Brazil, and Colombia. A core strength. | Focus on US payment rail depth. International payouts currently available via stablecoins. SWIFT coming soon. |

| Real-time ledger & reconciliation | Reconciliation typically requires additional systems for treasury operations. | A real-time double-entry ledger and automated reconciliation, the ledger behind $600B+ in payments. |

| Card issuing | Virtual card issuance supported. | Not a card issuer. Pair with a card issuer where cards are needed. |

| Bank model | Funds move within Bridge's stablecoin infrastructure and partner network. | Start with our payment service provider, or bring your own bank and operate across multiple institutions. |

Where the Approaches Differ

Stablecoin-first vs. bank-native

Bridge is built stablecoin-first, with issuance and on/off-ramps as core products. Modern Treasury is bank-native, treating stablecoins as one orchestrated rail alongside deep US bank rails.

Native ACH pull and instant rails

Bridge supports FedNow but not RTP, and native ACH pull is not evidenced. Modern Treasury originates ACH credits and debits, pulls funds directly from customer bank accounts, and runs RTP and FedNow as first-class rails.

Bank connectivity built in

Bridge does not offer bank-account connectivity or verification. Modern Treasury verifies and links customer bank accounts inside the same flow, using micro-deposits, prenote, and a built-in Plaid integration.

Ledger and reconciliation depth

Bridge typically needs additional systems for treasury operations. Modern Treasury centers on a real-time double-entry ledger with reconciliation and payment operations across every rail.

Different Platforms, Different Infrastructure

Bridge is best for:

- Stablecoin issuance as a core product requirement

- Virtual card issuance

- Local payment rails in Europe or Latin America

- Cross-border money movement where stablecoins are the rail

- Products centered on stablecoin rails rather than deep US bank operations

Modern Treasury is best for:

- Platforms that need ACH pull to collect funds from bank accounts

- Products where bank connectivity and account verification are core

- Teams that need RTP, FedNow, ACH, wire, and stablecoins through one API

- Programmable sub-accounts with a real-time double-entry ledger

- One orchestration layer across both bank rails and stablecoins

Payments Processed

Across Fiat and Stablecoins

Not Months to Go Live

Common Questions About Modern Treasury vs. Bridge

Bridge and Modern Treasury both support stablecoin payments, but they serve different infrastructure needs. Bridge is stablecoin-first: stablecoin orchestration, issuance, on/off-ramps, and global payouts, with local rails in several European and Latin American markets. Modern Treasury is bank-native payment operations infrastructure that moves money across ACH (including pull), RTP, FedNow, wire, and stablecoins through a single API, with a real-time double-entry ledger, reconciliation, and bank connectivity built in.

Native ACH pull is not evidenced in Bridge's product; its ACH capabilities read as settlement-oriented. Modern Treasury supports ACH pull, so businesses can collect funds directly from customer bank accounts for account funding, recurring payments, subscriptions, and bank-to-bank transfers.

Modern Treasury supports both the RTP network and the FedNow Service for real-time bank payments in the United States. Bridge supports FedNow but not RTP.

Yes. Modern Treasury includes bank connectivity and account verification, so businesses can connect customer bank accounts and initiate payment flows through one platform rather than integrating separate providers. Bridge does not offer bank connectivity.

Bridge supports stablecoin issuance as a core product. Modern Treasury is not a stablecoin issuer; it orchestrates USDC movement on the same API as its fiat rails, with reconciliation across both.

Choose Modern Treasury when you need to collect funds with ACH pull, connect and verify customer bank accounts, run ACH, wire, RTP, FedNow, and stablecoins through one API, and manage reconciliation and payment operations on a real-time ledger. Bridge may be the better fit when your primary requirement is stablecoin issuance, virtual card issuance, or local payment rails in Europe, Mexico, Colombia, or Brazil.