Modern Treasury vs. Moov

Feature Comparison

| Capability | Moov | Modern Treasury |

|---|---|---|

| Primary use case | US card acquiring, bank payments, wallets, and payouts through one integration and one contract, built for technical teams. | Payment operations for B2B platforms moving money across ACH, RTP, FedNow, wire, and stablecoins over the bank accounts you choose. |

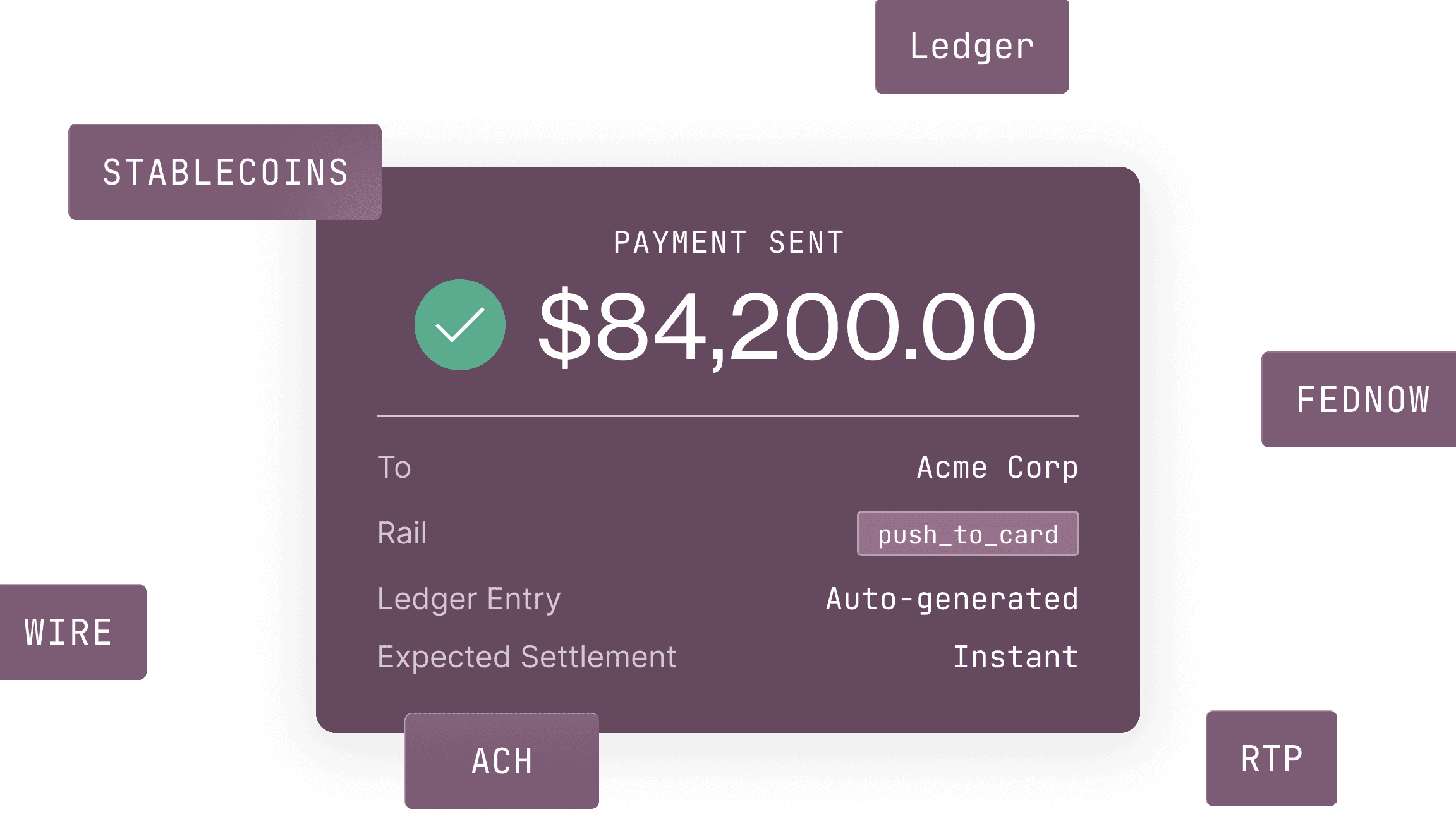

| Payment rails | Card acceptance, ACH credits and debits, same-day ACH, RTP, and push-to-card. Wire is not offered and FedNow is on the roadmap. | ACH, RTP, FedNow, wire, and stablecoins (USDC) as first-class rails on a single API. |

| Card acquiring & issuing | First-class card acceptance (online, Tap to Pay, digital wallets) at interchange-plus, plus Visa commercial debit card issuing. | Not a card acquirer. Modern Treasury moves money over bank rails; pair it with a card processor where cards are needed. |

| Wire transfers | Not part of the product. | Domestic and international wires on the same API as ACH and instant rails. |

| Stablecoins | No stablecoin or USDC support in the product, pricing, or docs. | Native USDC support across the same API as fiat rails. |

| Bank model | Integrated processor connected to the networks through its own FI partner banks; funds sit in Moov wallets. Not a bring-your-own-bank model. | Start with our payment service provider, or bring your own bank and operate across multiple institutions. |

| Real-time ledger | Real-time source-of-truth ledger with wallets that auto-correlate transactions to their original payment method. | A real-time double-entry ledger and automated reconciliation across banks, rails, and internal accounts, the ledger behind $600B+ in payments. |

| Programmable sub-accounts | Per-user accounts and up to 10 wallets each with balance automations, but no dedicated sub-account primitive. | Programmable sub-accounts designed to model funds, balances, and flows across entities in your system. |

| KYC / KYB / AML | Fully managed, brandable hosted onboarding with KYC, KYB, watchlist screening, and ongoing monitoring. | Use Modern Treasury's compliance tooling, or bring your own KYC/KYB/AML program. |

Where the Approaches Differ

Card acquiring vs. payment operations

Moov leads with card acceptance and card issuing as core products. Modern Treasury centers on bank-rail money movement, a real-time ledger, and reconciliation over the accounts you control.

Bring-your-own-bank vs. integrated processor

Moov is a single integrated processor whose FI partner banks sit inside its stack. Modern Treasury connects to your own bank relationships and can orchestrate across multiple institutions.

Rail breadth and geography

Moov's money movement is US-only, with no wire and no stablecoins, and FedNow still on the roadmap. Modern Treasury runs ACH, RTP, FedNow, wire, and stablecoins (USDC) as first-class rails today.

Compliance flexibility

Moov's KYC/KYB/AML is a single fully managed hosted flow. Modern Treasury gives you built-in compliance or the option to bring your own KYC/KYB/AML providers.

Different Platforms, Different Infrastructure

Moov is best for:

- US platforms that need card acquiring as a first-class rail

- Teams that want one integration and one contract across the stack

- Stored-value and wallet use cases with a built-in ledger

- Fully managed, hosted KYC/KYB onboarding

- US-domestic ACH, RTP, and push-to-card money movement

Modern Treasury is best for:

- B2B platforms moving money across bank rails at scale

- Teams that need wire and stablecoins alongside ACH and instant rails

- Platforms that want to bring their own bank or run multiple banks

- Programmable sub-accounts with a real-time double-entry ledger

- Companies that need one platform for fiat and stablecoins

Payments Processed

Across Fiat and Stablecoins

Not Months to Go Live

Common Questions About Modern Treasury vs. Moov

Moov is a US payments platform that combines card acquiring, bank payments, wallets, and payouts through one integration and one contract, built for technical teams. Modern Treasury is payment operations infrastructure for B2B platforms moving money over bank rails (ACH, RTP, FedNow, wire, and stablecoins) with a real-time double-entry ledger, reconciliation, and a bring-your-own-bank model. Moov leans toward card acceptance and stored-value wallets; Modern Treasury leans toward bank-rail money movement and treasury operations.

No. As of this research, Moov's public product, pricing, and docs make no mention of stablecoins or USDC; money movement runs over ACH, RTP, and card rails. Modern Treasury supports stablecoin and USDC flows on the same API as its fiat rails.

Wire transfers are not offered by Moov. FedNow is on Moov's roadmap but is not yet a general capability; ACH, same-day ACH, RTP, and push-to-card are live. Modern Treasury supports ACH, RTP, FedNow, and wire today.

No. Modern Treasury moves money over bank rails and is not a card acquirer. If your platform needs to accept cards, many teams pair a card processor for acceptance with Modern Treasury for ACH, wire, instant, and stablecoin money movement, plus ledgering and reconciliation.

Funds are held in Moov wallets under Moov's model as a licensed processor connected to the payment networks through its FI partner banks. Modern Treasury uses a bring-your-own-bank model, so funds stay in your own bank accounts and you keep the bank relationship.

Choose Moov if you are a US software platform whose primary need is card acquiring or card issuing alongside bank rails, and you want one vendor, one contract, and a fully managed wallet and hosted-onboarding stack without bringing your own bank. Choose Modern Treasury if you need to keep your own bank relationships, require wire or stablecoin rails, or want a programmable double-entry ledger and reconciliation over accounts you control.