Modern Treasury vs. Plaid

Feature Comparison

| Capability | Plaid | Modern Treasury |

|---|---|---|

| Primary use case | Bank-account connectivity, data, and verification: linking accounts and turning bank data into financial products. | Payment operations: moving money across ACH, RTP, FedNow, wire, and stablecoins with a real-time ledger and reconciliation. |

| Account connectivity & verification | Core strength: Auth verifies account and routing numbers, Balance returns real-time balances, and Identity matches account-holder details across 12,000+ institutions. | Includes bank connectivity and account verification, but connectivity is one input to payment operations rather than the core product. |

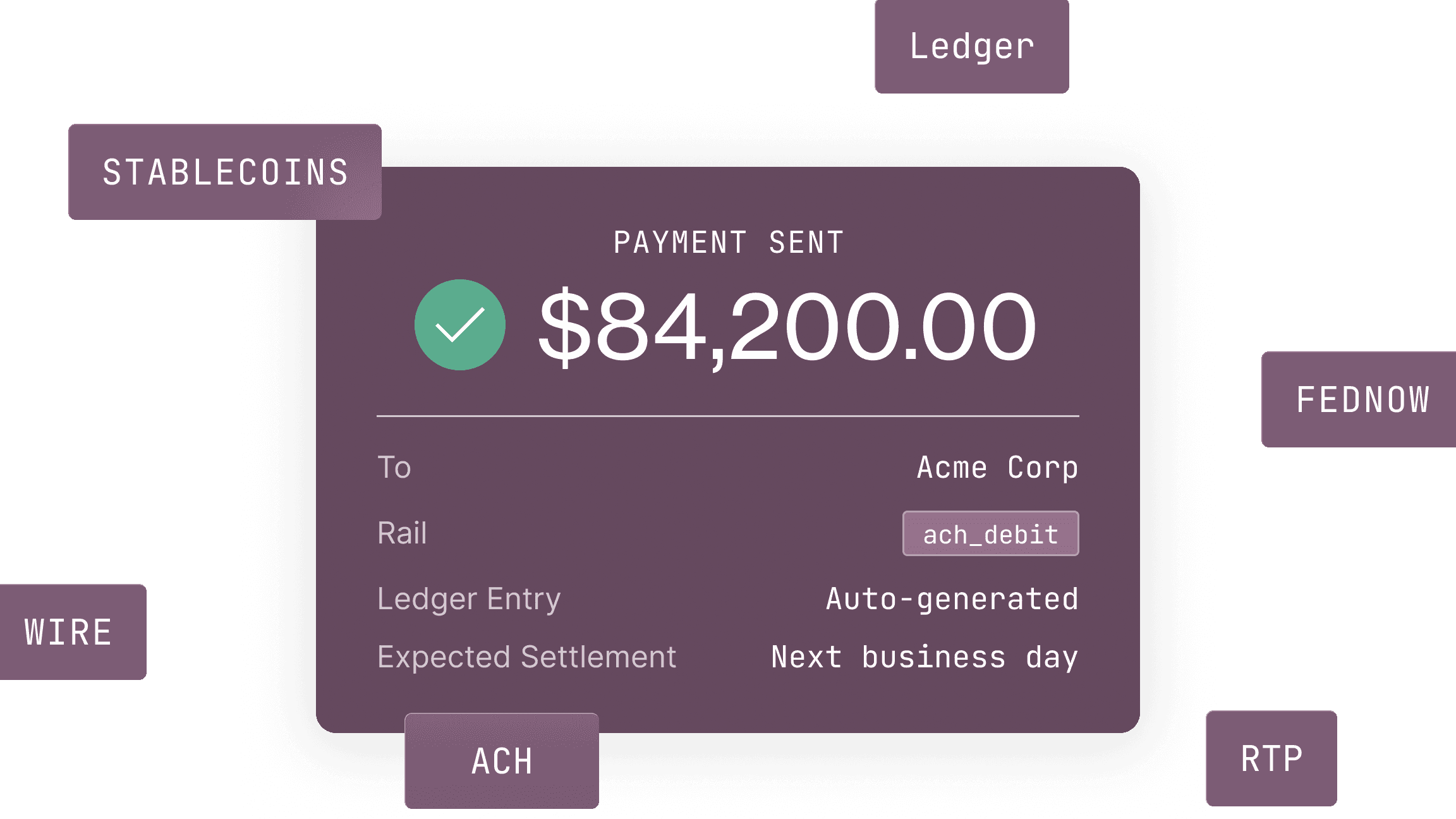

| Payment rails / money movement | Plaid Transfer moves money over ACH (credit + debit), Same-Day ACH, RTP, FedNow, RfP, and wire. US-only, with no push-to-card or stablecoins. | ACH, RTP, FedNow, wire, and stablecoins (USDC) as first-class rails on a single API. |

| Stablecoins | No stablecoin or USDC capability documented. | Native USDC support across the same API as fiat rails. |

| Real-time double-entry ledger | Plaid Transfer includes a single “Plaid Ledger” balance with sweeps and reconciliation reports, not a double-entry ledger of record. | A real-time double-entry ledger tracking balances and entries across entities, the ledger behind $600B+ in payments. |

| Programmable sub-accounts | A single Ledger balance with sweeps; no programmable per-end-customer sub-account model documented. | Programmable sub-accounts designed to model funds, balances, and flows across entities in your system. |

| Fraud / identity products | Signal scores ACH return and fraud risk, Beacon is a shared anti-fraud network, and Identity Verification adds document and liveness checks. A core strength. | Focused on payment operations; fraud and identity are typically handled by dedicated tools such as Plaid alongside Modern Treasury. |

| KYC / AML screening | Global KYC via Identity Verification (document + liveness) and AML watchlist/sanctions/PEP screening via Monitor. | Use Modern Treasury's compliance tooling, or bring your own KYC/KYB/AML program. |

| Fund model | Verification-only for Auth (bring your own processor); for Transfer, funds flow through Plaid's own Ledger. | Bring-your-own-bank: orchestrates money movement over your own bank relationships. |

Where the Approaches Differ

Connectivity/data vs. payment operations

Plaid's foundation is linking and reading bank accounts and scoring risk. Modern Treasury's foundation is operating payments end to end, originating money movement, ledgering every dollar, and reconciling against bank activity.

Rail breadth and geography

Plaid Transfer is US-only and covers ACH, RTP, FedNow, RfP, and wire, with no push-to-card or stablecoins. Modern Treasury spans a broader rail set including stablecoins (USDC).

Ledger depth

Plaid's Ledger is a single funds-holding balance with sweeps and reconciliation reports. Modern Treasury provides a real-time double-entry ledger with programmable sub-accounts for tracking balances per entity.

Complementary by design

The two are often used together: Plaid links and verifies the account (and can screen fraud and identity), while Modern Treasury moves the money across rails, ledgers each transaction, and reconciles it.

Different Platforms, Different Infrastructure

Plaid is best for:

- Instant bank-account linking and verification

- Real-time balance and funding checks

- Account-owner identity matching and onboarding

- ACH and bank-payment fraud and return-risk scoring

- KYC and AML screening at onboarding

Modern Treasury is best for:

- Moving money across ACH, RTP, FedNow, wire, and stablecoins

- A real-time double-entry ledger and automated reconciliation

- Programmable sub-accounts and third-party fund management

- Bringing your own bank and running multiple banks

- Payment operations and treasury workflows at scale

Payments Processed

Across Fiat and Stablecoins

Not Months to Go Live

Common Questions About Modern Treasury vs. Plaid

Plaid is primarily bank-account connectivity, data, and verification, linking accounts (Auth), returning balances (Balance), matching identity (Identity), and scoring fraud and risk (Signal, Beacon), and it now moves money in the US via Plaid Transfer. Modern Treasury is payment operations infrastructure: it moves money across ACH, RTP, FedNow, wire, and stablecoins, ledgers every transaction in a real-time double-entry ledger, and reconciles it. The two are often complementary rather than competitive.

Yes. Plaid Transfer is a US-only, multi-rail API supporting ACH (debit and credit), Same-Day ACH, RTP, FedNow, Request for Payment, and wire, with a Plaid Ledger balance for holding and sweeping funds. It does not document push-to-card or stablecoin rails. Modern Treasury supports a broader rail set including stablecoins.

Plaid Transfer includes a single “Plaid Ledger” balance with sweeps and reconciliation reports, but not a real-time double-entry ledger with programmable sub-accounts for tracking balances per end customer. Modern Treasury centers on a double-entry ledger of record.

Yes, and they're commonly complementary. A typical pattern: Plaid links and verifies the bank account (and can screen fraud and identity at onboarding), while Modern Treasury moves the money across rails, ledgers every transaction, and reconciles it. Using both lets each system do what it's built for.

Reach for Plaid when your core need is linking bank accounts, verifying account and routing numbers and balances, matching account-owner identity, running KYC/AML at onboarding, or scoring ACH and fraud risk, the connectivity, data, and verification layer. Reach for Modern Treasury when you need to move money across many rails, maintain a real-time double-entry ledger, manage sub-accounts or third-party funds, and reconcile at scale.

Modern Treasury includes bank connectivity and account verification, but as inputs to payment operations rather than as the core product. Many teams still use Plaid for the deepest connectivity, identity, and risk coverage, and pair it with Modern Treasury for money movement, ledgering, and reconciliation.