The Stablecoin Sandwich vs. Traditional Cross-Border Payments

Feature Comparison

| Capability | Traditional Cross-Border Payments | Stablecoin Sandwich (Modern Treasury) |

|---|---|---|

| Settlement speed | Payments can take days depending on intermediaries, cutoffs, and local banking systems | Near real-time movement of funds globally |

| Infrastructure | Built on correspondent banking networks and intermediaries | Fiat on-ramp → stablecoin transfer → fiat off-ramp |

| Liquidity management | Requires pre-funding accounts across countries and banking partners | Move liquidity globally without parking capital in every market |

| Visibility | Limited tracking once payments move across intermediary banks | Real-time visibility across payment and settlement flows |

| Reconciliation | Fragmented across banks, FX providers, and payout systems | Unified ledger and reconciliation across fiat and stablecoin rails |

| Expansion into new markets | New corridors often require new banking and operational infrastructure | Launch faster without rebuilding your payment stack |

| Native stablecoin support | Usually unsupported or handled through separate crypto vendors | Native USDG, USDC, and USDT support through the same API and platform |

| Operational overhead | Multiple providers, disconnected systems, manual workflows | One orchestration layer across fiat and stablecoin payments |

| Fiat & stablecoin orchestration | Not part of most processors' core platforms. | USDG, USDC, and USDT run on the same platform as fiat. No separate integration required. |

| Ongoing maintenance | Bank changes, compliance updates, and rail certifications are your team's responsibility. | Handled by Modern Treasury. Your team focuses on your product. |

Where Traditional Cross-Border Payments Break Down

Settlement timelines slow everything down

Payments routed through correspondent banks and local clearing systems arrive slowly, with limited visibility and unpredictable liquidity. The stablecoin sandwich replaces that chain with a faster, more transparent movement layer.

Liquidity gets trapped across markets

Scaling globally means pre-funding accounts in every market, leaving capital idle across jurisdictions. Stablecoin-based settlement keeps liquidity mobile and deployable across borders.

Reconciliation becomes an operations problem

High-volume cross-border flows fragment records across banks, FX providers, and internal systems. Modern Treasury unifies fiat and stablecoin reconciliation in a real-time, double-entry ledger.

Expanding globally gets operationally expensive

Each new corridor brings new bank relationships, compliance workflows, and systems to manage. The stablecoin sandwich standardizes the movement layer, making expansion lighter to operate.

Payments Processed

Across Fiat and Stablecoins

Not Months to Go Live

Different Platforms, Different Infrastructure

Traditional cross-border payments work well when:

- Payment volume is low

- Settlement speed is not business-critical

- Existing banking relationships meet your needs

- Manual reconciliation is manageable

- Real-time liquidity isn't a priority

The stablecoin sandwich is the right fit when:

- Faster settlement improves customer or treasury outcomes

- You operate across multiple countries or currencies

- Liquidity needs to move efficiently across markets

- Reconciliation is becoming a bottleneck

- You want a single infrastructure layer across fiat and stablecoin rails

- You need to add corridors without rebuilding your stack

Common Questions About the Stablecoin Sandwich

The stablecoin sandwich is a three-step cross-border payment model: fiat is converted into a stablecoin (typically USDC or USDT), the stablecoin moves on a blockchain to the destination region, and the stablecoin is converted back into local fiat for payout. The model replaces correspondent banking with near-instant settlement and keeps liquidity mobile across markets.

Stablecoins can reduce settlement times, improve liquidity mobility, and lower operational overhead compared to traditional correspondent banking systems. They also provide more visibility into payment flows and simplify reconciliation across global payment operations.

No. Most businesses still rely on banks for local accounts, payouts, compliance, and fiat custody. In practice, stablecoins and banking rails increasingly operate together as part of the same payment infrastructure stack.

The stablecoin sandwich becomes more compelling as businesses scale internationally and operational complexity increases. Faster settlement, better liquidity efficiency, and simpler reconciliation can meaningfully improve cross-border payment operations.

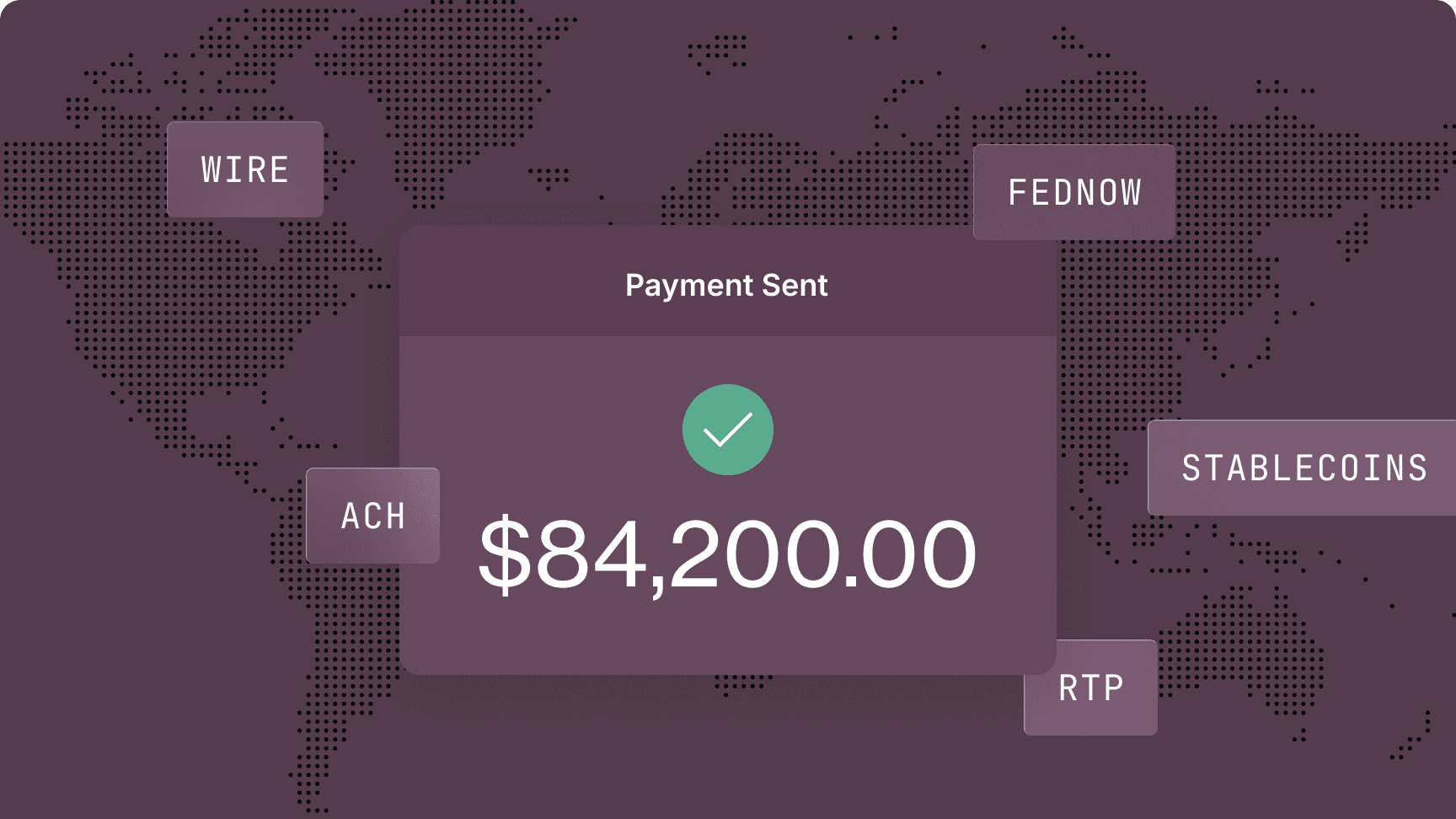

Modern Treasury supports ACH, wire, RTP, FedNow, push-to-card, and stablecoin rails through a single Payments API. Businesses can orchestrate fiat and stablecoin payment flows through one platform instead of managing separate systems and providers.

Yes. Many businesses use stablecoins for settlement and liquidity movement while continuing to use traditional banking rails for local collection and payouts. Modern Treasury supports both models through the same infrastructure layer.

Yes. Stablecoins can be a safe and reliable payment method for businesses when issued by reputable providers and supported by strong operational controls. Modern Treasury helps companies manage stablecoin payments with enterprise-grade approval workflows, reconciliation, compliance monitoring, and reporting. Growing regulatory clarity through frameworks such as the GENIUS Act in the U.S. and MiCA in Europe is helping establish standards for stablecoin reserves, transparency, and consumer protections.

Stablecoin payments and cross-border wire transfers both enable international money movement, but they differ in speed, cost, and availability. Stablecoin payments can settle in minutes, 24/7, while traditional international wire transfers often take several business days and rely on intermediary banks. Through Modern Treasury, businesses can use stablecoins for cross-border payments to improve settlement speed, payment visibility, and operational efficiency. Many companies support both payment rails, using stablecoins for faster global payments and wires when bank-to-bank transfers are required.