A Practical Guide to PSPs in 2026

How modern payment service providers are evolving to manage the full lifecycle of money movement.

April 13, 2026

15 minutes

Contents

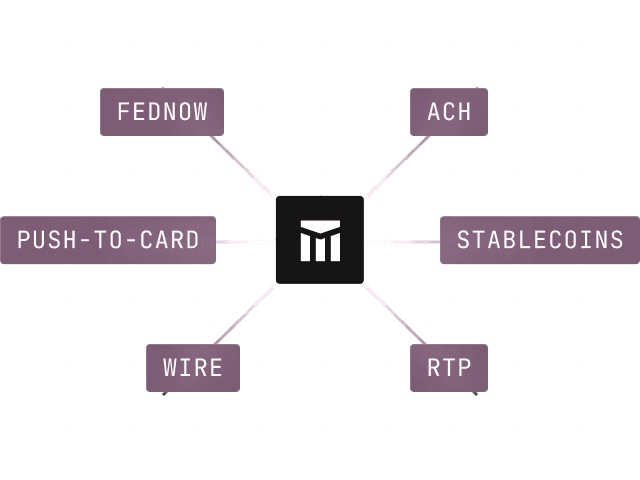

Modern Treasury connects fiat and stablecoin rails in one API.

The expanding role of Payment Service Providers

Payment service providers have evolved from payment acceptance tools into the core infrastructure layer that governs how money moves, settles, and is ledgered. They were originally designed for a simpler era of payments that was defined by single-rail systems, linear transaction flows, and tightly bundled infrastructure.

Legacy payment service providers were built to solve a relatively narrow problem: helping businesses accept payments. They were optimized to authorize, capture, and settle payments through specific rails, most commonly card networks.

This architecture worked well for its time when payments were linear and confined to a single provider. However, it becomes harder to extend as payments grow more complex to span multiple steps, participants, and rails.

In modern payment environments, a single "payment" is no longer a single transaction. It is a sequence of state transitions across multiple providers and payment rails, and PSPs must now manage that sequence with a consistent, end-to-end view.

Today, a single payment may involve a user-facing application, a PSP, a fraud or identity provider, a sponsor bank, one or more payment rails, and a company's internal system of record that ledgers what happened after funds move.

We're in the middle of a broader change in how businesses move money. Companies no longer operate on a single rail or through a single provider. They must support cards, ACH, wires, RTP, FedNow, and increasingly stablecoin-based settlement.

Each rail introduces different timing, failure modes, data formats, and operational requirements. As a result, the infrastructure required to manage and explain money movement has become more complex and raised expectations for PSPs.

This guide examines how PSPs evolved, how their underlying architecture needs to adapt to modern payment systems, and how teams building payment products should approach their next PSP.

How payment service providers evolved

The role of payment service providers has changed significantly during the past two decades.

In the early years of e-commerce, PSPs functioned mainly as payment gateways. Their responsibility was simple: connect merchants to card networks and acquiring banks so transactions could be authorized and settled.

These PSP systems were designed for a very specific world. Payments were primarily card-based, flowed through a single merchant account, and followed a linear lifecycle from authorization to settlement. PSPs were optimized to process transactions efficiently within that model.

As digital commerce expanded during the 2010s, new business models emerged that required more advanced payment infrastructure. Marketplaces, SaaS platforms, and fintech products began to embed payments directly into their products. Instead of a single merchant accepting payment, platforms needed to onboard users, split payments across multiple parties, and manage payouts.

PSPs expanded accordingly. They introduced merchant onboarding, payout infrastructure, and fraud prevention tools to support these new use cases.

However, while PSP capabilities expanded, their underlying architecture remained rooted in a model designed for linear payment flows. Most PSPs were still primarily optimized for transaction processing rather than coordinating complex, multi-step money movement across providers and payment rails.

By the early 2020s, payments evolved again. Businesses began to operate across multiple rails, geographies, and use cases, with each introducing new requirements around compliance, banking relationships, and settlement.

Legacy PSPs continued to bundle many of these components within a single product. These components, which are typically abstracted away from the user, allow businesses to interact with a single platform instead of managing each dependency directly. As payment flows become more complex, these bundled architectures require workflows that extend beyond their original design.

A single payment flow may now span multiple steps and dependencies, such as identity verification, risk checks, funding decisions, execution across a payment rail, and internal tracking of balances and state.

**This shift changed the role of PSPs from connectors to coordinators, but their architecture did not evolve at the same pace. **As a result, PSPs remain responsible for moving money, but must now operate in environments where the full lifecycle of a payment is harder to manage.

Understanding that shift is key to understanding modern PSP stacks.

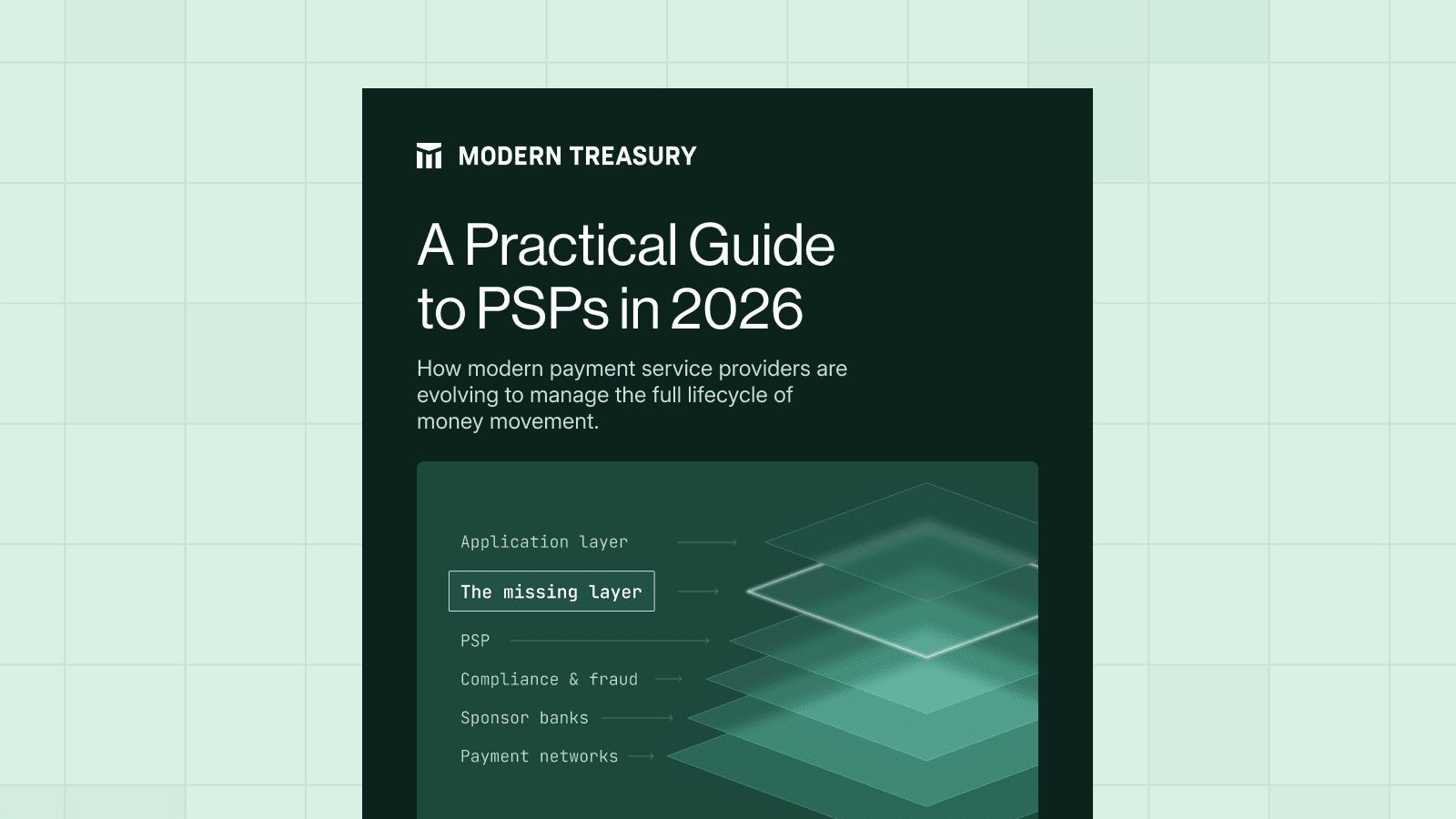

Inside the modern PSP stack

To understand the limits of payment service providers, it is necessary to understand the broader payment environment they operate within.

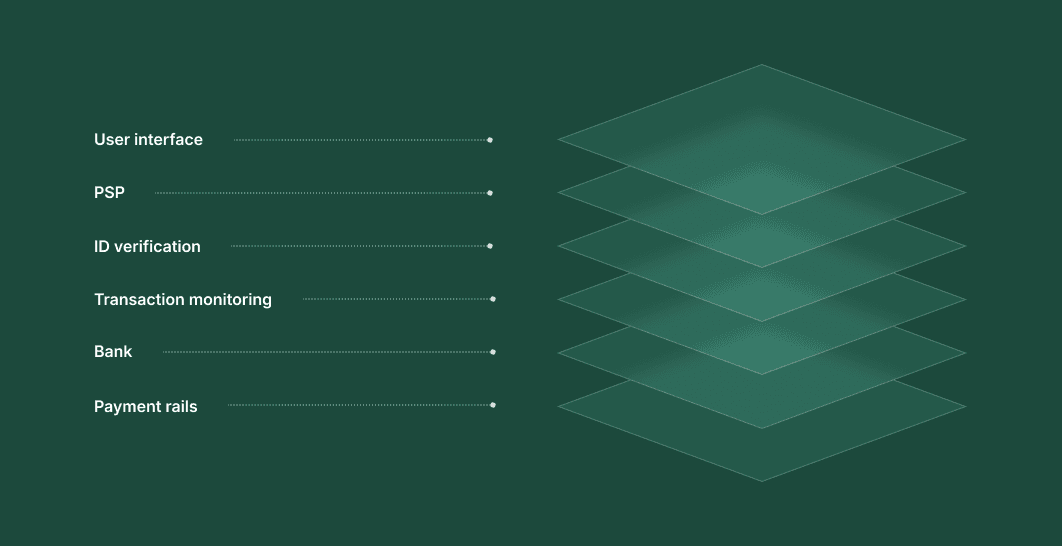

Modern payment environments are not a single platform or provider. They are a layered set of infrastructure components that together enable money to move, settle, and be ledgered.

At the top of the stack are the applications where payments originate. These include e-commerce platforms, marketplaces, fintech apps, and SaaS products that embed payments into the user experience.

Below this layer sit payment service providers. PSPs are responsible for executing payment instructions such as routing transactions to card networks, initiating bank transfers, and interfacing with payment rails.

PSPs operate as systems of action. They move money, but they do not operate alone. In most cases, this underlying complexity is abstracted behind the PSP's interface, so users interact with a single system rather than the multiple providers involved under the hood.

A modern payment flow also depends on identity verification providers, fraud detection tools, and compliance infrastructure. These systems determine whether a payment should be allowed to proceed.

Banks form another critical layer. Sponsor banks hold funds, provide regulated accounts, and enable access to payment networks such as ACH, wires, RTP, and FedNow.

Each of these components plays a role in moving money. But none of them, including legacy PSP architecture, provides a complete picture of what happens after a payment is initiated.

This is where the internal reconciliation layer becomes essential. The internal reconciliation layer is a system a business uses to track balances, represent transaction state, and maintain a consistent record of financial activity over time.

This layer is not an extension of the PSP. It exists because the internal architectures PSPs were originally designed around were not built to maintain a complete, system-wide view of today's payment flows.

One of the core limitations of legacy PSPs is that they do not maintain a full representation of transaction state across the entire lifecycle of a payment, especially across multi-rail payments.

Each provider exposes its own status model, timing, and event structure. A payment may be marked as "completed" by a processor while still being reversible on the underlying rail. A bank may report settlement after a company's internal systems have already updated balances. Returns, reversals, and adjustments often arrive asynchronously.

The result is state fragmentation. The same payment can exist in multiple states at once, depending on which provider or system you query.

Most PSPs expose APIs for initiating payments, but they are not designed to serve as systems of record across all providers and internal systems involved. Their APIs reflect the lifecycle of transactions within their own environment, not the full lifecycle of funds movement across banks, rails, and internal ledgers, creating a fundamental mismatch.

PSP interfaces are largely synchronous. A request is made, and a response is returned.

But real-world payment systems are asynchronous. Settlement occurs later. Failures surface after initiation. External providers and networks introduce delays and reorder events. This mismatch creates a gap between what systems report in real time and what actually happens to money over time.

Consider a marketplace payout.

A seller requests a withdrawal. The platform verifies eligibility. Fraud and compliance checks run. Funds availability is confirmed. A payment instruction is sent through a PSP to a bank partner over a chosen rail. A confirmation event is returned. Settlement occurs later. The platform updates the seller's balance and records the transfer. If that payout fails, is delayed, or is returned, the system must determine what to show the user, how to update balances, and whether the external event matches internal ledgers.

Even when a PSP supports large portions of this flow, the full lifecycle of the payment extends beyond any single provider's internal system.

This is the core limitation of traditional PSP architectures. They execute payments, but were not designed to provide a real-time, unified, and system-wide understanding of how money moves across providers and internal systems over time. That challenge becomes even harder to manage as payments span multiple rails, each with its own behavior, timing, and guarantees.

To understand why this problem compounds, it is necessary to look at how payment rails differ.

When payment rails break the PSP abstraction

One of the defining challenges for modern payment service providers is that they no longer provide a consistent or reliable view of payment state.

A payment that appears "complete" in one system may still be reversible, pending, or subject to failure in another. As payment flows extend across multiple rails and providers, the ability to represent a single, authoritative state becomes increasingly difficult.

The issue isn't simply the increase in payment rails, but that each rail introduces its own distinct behavior and assumptions.

Traditional PSP abstractions were built around card payments, where transactions follow a relatively consistent lifecycle. A payment is authorized, captured, and settled. While there are exceptions such as disputes and chargebacks, the overall structure is predictable and well understood.

This model shaped how PSPs were designed.

As new payment methods emerged, PSPs extended support to additional rails. But these rails do not behave like cards, and they do not conform to the same assumptions.

ACH transfers introduce delays and the possibility of returns days after a payment is initiated. Wires provide faster settlement but often require manual processes and higher costs. Real-time payment networks such as RTP and FedNow enable immediate movement of funds, but transactions are typically irreversible once completed. Stablecoin-based transfers operate on entirely different infrastructure, with different guarantees and operational considerations.

These are not variations of the same payment model. They are fundamentally different operational models. For PSPs, this creates a structural challenge.

The abstractions that worked for card payments do not generalize cleanly across rails. Instead of providing a unified model, legacy PSP abstractions often expose rail-specific behaviors through different APIs, workflows, and status definitions, which leads to abstraction leakage.

As businesses support more payment methods, the differences between rails surface at the application layer. Engineering teams must account for different settlement timelines. Operations teams must handle different failure modes. Finance teams must reconcile transactions that follow different paths to finality.

A payment marked as "complete" on one rail may still be reversible. A payment on another rail may settle instantly with no ability to recover funds. A third may appear pending for days before final resolution.

To a PSP, these may all be represented as payments. To a business, they require entirely different handling. As a result, companies begin to implement rail-specific logic throughout their internal systems by handling retries, managing exceptions, and interpreting statuses differently depending on how the payment was executed.

This is where the traditional PSP model begins to show its limits.

PSPs can connect businesses to multiple rails, but the abstractions they were originally designed around do not provide a consistent way to reason about how those rails behave.

As more rails are added, the payment environment becomes a collection of loosely connected integrations rather than a unified abstraction. And as that complexity grows, the limitations of the legacy PSP architecture become more visible.

On slower rails, delays and reversibility create time to detect issues, reconcile differences, and intervene before settlement is final. On real-time rails, that margin disappears. Payments settle within seconds. Errors cannot be reversed easily. Decisions must be made before funds move, not after.

This is where the limitations of legacy PSP abstractions become unavoidable, and where the design of payment systems must fundamentally evolve.

Real-time payments force PSPs to move control upstream

One of the defining challenges for modern payment service providers is that they no longer provide a consistent or reliable view of payment state.

The shift to real-time payment networks does more than increase the speed of money movement. It fundamentally changes how payment infrastructure needs to be designed and what is required of payment service providers.

On traditional rails, time acts as a buffer.

ACH payments may take days to settle. Card transactions can be disputed after authorization. Even wires, while faster, often involve manual steps and review processes. These delays introduce inefficiencies, but they also create opportunities to detect errors, intervene in suspicious activity, and reconcile inconsistencies before settlement becomes final.

Legacy PSP models were built around this buffer.

They assume that some level of review, correction, or reconciliation can happen after a payment is initiated. If something goes wrong, there is often time to respond before funds are permanently moved.

Real-time payment networks remove that assumption.

Networks such as RTP and FedNow allow funds to move directly between accounts within seconds. Once a payment is completed, it is typically final and irreversible.

Decisions that could previously happen after initiation must now happen before execution. Fraud checks must be completed earlier. Compliance screening must happen in real time. Funding decisions must be accurate at the moment a payment is released. There is no opportunity to correct errors after the fact.

Most legacy PSP architectures were designed to initiate and track payments, not to enforce upstream decision-making. They rely on downstream processes such as reconciliation, exception handling, and manual review to resolve issues that arise during payment execution. It's a model that does not hold in a real-time environment.

A platform offering instant payouts cannot depend on workflows designed for delayed settlement. A company's internal system for funding payments from multiple accounts cannot determine liquidity at the moment of execution. A support team cannot promise reversibility when the underlying rail does not allow it.

The result is a shift in responsibility. PSPs must evolve to support internal systems that determine when a payment should be executed in the first place. In other words, control must move upstream.

Payment infrastructure must be designed so that approvals, funding logic, risk checks, and state validation happen before funds move, not after. This requires a more coordinated view of balances, transaction state, and conditions across providers and internal systems than traditional PSP architectures were designed to provide.

And real-time bank rails are not the end state of this evolution. New forms of payments are emerging that operate outside traditional banking systems entirely, with different assumptions about settlement, finality, and control. These systems introduce another layer of complexity by extending the challenge of coordinating money movement across rails that do not share the same underlying model.

To understand where PSPs are heading, it is necessary to look beyond traditional rails and examine how these new networks fit into the broader ecosystem.

Stablecoins extend the PSP challenge beyond traditional rails

As payment infrastructure expands beyond traditional banking systems, stablecoins introduce a new dimension to the role of payment service providers.

Unlike card networks, ACH, or real-time bank rails, stablecoin transactions operate on blockchain-based networks. These networks are designed to maintain a stable value relative to fiat currencies while enabling funds to move across digital infrastructure that sits outside the traditional banking system.

For PSPs, this introduces a fundamentally different model for how money moves, settles, and is ledgered.

Stablecoin transactions can settle continuously rather than in batches. They may offer near-instant finality, depending on the network. They operate across global infrastructure rather than being tied to a specific domestic payment system. And they expose a different set of primitives for tracking balances, ownership, and transaction history.

Just as real-time payment systems challenged assumptions about timing and reversibility, stablecoins challenge assumptions about where payments happen and how they are represented. In doing so, they introduce a new layer of complexity.

Traditional PSP architectures were built around integrations with banks and payment networks. Stablecoins introduce networks that do not rely on those same intermediaries. This means PSPs must now account for payment flows that originate, settle, and are ledgered outside the infrastructure they were originally designed to connect to.

This further expands the problem introduced in earlier chapters: payment systems are no longer just multi-rail. Now, they span multiple types of infrastructure.

A single business may now need to coordinate payments across bank-based rails, real-time networks, and blockchain-based settlement networks, each with different assumptions about finality, timing, and control.

As a result, the abstractions PSPs were originally designed around become harder to maintain.

A stablecoin transfer may settle instantly with cryptographic finality. A bank-based payment may still be subject to returns or reversals. A real-time payment may be final but dependent on bank network availability. These differences are not easily unified through a single API or status model. Instead, businesses must reason about each environment independently.

For PSPs, this means the challenge is no longer limited to supporting multiple rails within the banking system. It now includes coordinating across fundamentally different types of financial infrastructure.

As new rails are added, the responsibilities involved in moving money become further distributed across different environments and providers. Execution, settlement, custody, and recordkeeping may each occur in different environments, with different guarantees and timelines.

The PSP, as a single unified abstraction, is becoming increasingly difficult to maintain in this environment. As a result, it becomes necessary to understand how these responsibilities are divided and how the providers that support them fit together.

How PSP responsibilities are distributed across modern payment systems

As payment infrastructure expands across more rails, more providers, and more forms of infrastructure, the role of the payment service provider becomes increasingly difficult to define.

What was once bundled within a single PSP for moving money is now a set of responsibilities distributed across multiple layers of the stack.

The job of a PSP is no longer just to move money. It is to explain money movement.

This shift reflects a deeper change: execution alone is no longer sufficient. PSPs must now support a company's internal system that can represent, ledger, and reconcile how money moves across different environments.

1. Product-layer platforms: embedding payments into software

Vertical software platforms such as Shopify, Square, Toast, Mindbody, ServiceTitan, and Housecall Pro embed payments directly into their products.

In these cases, payments are integrated into the application experience rather than treated as a separate payment system.

These platforms often rely on underlying PSPs, banking partners, and infrastructure providers by adding another layer of abstraction between the application and the movement of funds.

2. Execution: money movement across rails

At the core are providers responsible for executing payments.

These include traditional PSPs such as Stripe, Adyen, Checkout.com, Worldpay, PayPal, Nuvei, and dLocal. Their role is to connect businesses to payment rails and facilitate the movement of funds.

They remain a critical part of the payment stack. But they operate primarily within the execution layer. They initiate payments, report statuses, and expose APIs.

They do not, on their own, provide a complete model of how money moves across providers and internal systems.

3. Orchestration and routing: connecting execution providers

As businesses adopt multiple PSPs and payment methods, orchestration platforms emerge to manage routing across providers.

Companies such as Primer, Gr4vy, Spreedly, Paydock, and CellPoint Digital allow businesses to direct transactions based on geography, cost, or performance.

These systems improve flexibility at the execution layer, but they do not provide a unified model for how payments behave after they are initiated.

4. Risk and compliance: deciding whether money should move

A separate set of providers is responsible for determining whether a payment should be allowed to proceed.

Identity verification, fraud detection, and compliance systems happen through vendors such as Persona, Sardine, Alloy, Unit21, Sift, and Sumsub. They evaluate users and transactions before execution.

In a real-time environment, these decisions must happen before funds move, and this shifts critical control logic outside the PSP itself.

5. Banking infrastructure: holding funds and enabling access

Sponsor banks such as Cross River Bank, Lead Bank, Column, and Sutton Bank provide regulated accounts and access to payment networks.

They hold customer funds, manage liquidity, and serve as the gateway to rails such as ACH, wires, RTP, and FedNow.

This layer is essential for accessing the financial system, but it operates independently from both application logic and PSP APIs.

6. Card issuing: extending payment functionality

Card-issuing platforms such as Marqeta, Lithic, and Rain enable businesses to issue debit and credit cards as part of their offerings.

These systems allow companies to embed spend directly into their platforms, supporting use cases such as expense management, corporate cards, and marketplace spending.

While issuing platforms connect to banks and card networks, they operate as a distinct layer within the stack by introducing additional workflows, controls, and state that must be coordinated alongside other parts of the payment stack.

7. Payment rails: the underlying execution layer

Payment rails are the networks that move funds between financial institutions.

Traditional rails include ACH, wires, and card networks, while newer networks such as RTP and FedNow enable real-time settlement.

Each rail operates with different assumptions around timing, finality, and reversibility, creating inconsistencies that PSPs must expose or work around rather than fully abstract.

8. Stablecoin networks: expanding beyond banking infrastructure

Stablecoin networks such as Ethereum, Solana, Polygon, and Base introduce a new form of payment infrastructure that operates outside traditional banking systems.

These networks enable the transfer of digital dollars across global infrastructure with different settlement models and guarantees.

They extend the scope of payment systems beyond bank-based rails, adding another layer of complexity that must be integrated into existing workflows.

9. Banking-as-a-service: connecting applications to banks

Banking-as-a-service platforms such as Unit, Galileo, and Treasury Prime provide the infrastructure that connects fintech applications to regulated banks.

They enable companies to offer accounts, cards, and payment capabilities without becoming banks themselves.

This layer simplifies access to banking infrastructure, but adds another intermediary between applications, PSPs, and the underlying movement of funds.

10. The missing layer: a unified PSP for the full lifecycle of money movement

Across all of these categories, one pattern becomes clear.

Each provider is responsible for a specific function. None of them, on their own, provides a complete view of money movement for understanding, controlling, and reconciling it.

Execution is handled by one provider. Risk decisions in another. Funds are held in a bank. Payment flows may extend across card networks, real-time rails, and blockchain-based systems. Each exposes different data, timelines, and definitions of state.

The PSP, as a unified abstraction, is becoming harder to maintain as payment systems grow more complex.

As a result, there is no consistent way to track transaction state across providers, manage workflows before and after execution, or maintain a reliable financial record of what actually happened to money as it moves.

As more providers are added, the complexity compounds. In a fragmented environment, no single provider can fully explain what happened to a payment. That problem does not appear at initiation. It appears later when systems disagree, when funds are delayed or returned, and when teams need answers. This is where payment systems begin to break down.

Where payment operations break

The hardest problems in payments often do not appear at initiation. They appear later, when teams need to explain what happened.

The market map in the previous section highlights how broad the payments ecosystem has become. What appears to be a single payment often moves through multiple providers across the stack before settlement occurs.

A business may initiate payments through one provider, hold funds with a banking partner, receive settlement reports from a network, and maintain internal records in a separate system. Each party may represent the same movement of money differently. Timing differs. Statuses differ. Files arrive on different schedules. Exceptions are reported through different channels.

That is where payment operations become difficult.

Reconciliation: multiple versions of the same event

Reconciliation is one of the clearest examples. Finance teams need to match internal ledgers against bank activity, settlement reports, processor data, and ledger balances. If one provider or system shows a payment as completed while another shows it as pending, the business needs a model for resolving that difference. If a return arrives after balances were updated internally, the business needs to reverse or adjust its ledgers. If multiple providers are involved, it needs to know which event should drive the internal source of truth.

Exception handling: failures without clear ownership

Exception handling is another common failure point. A payout may fail because the destination account is invalid, the wrong funding account was used, a compliance review placed a hold on the transaction, or a rail-specific cutoff was missed. Those failures are not all the same, and they do not all happen at the same time. But users still expect a coherent answer, and internal teams still need a process for responding.

Liquidity and funding: the right money in the wrong place

Liquidity and funding create a third layer of operational risk. A business operating across multiple providers and accounts has to ensure that the right funds are in the right places at the right times. If money is available overall but sits in the wrong account, payment execution can fail even when the broader balance picture looks healthy. This creates a gap between product logic and operational reality.

Auditability and control: reconstructing what happened

Then there is auditability and control. As approvals, holds, releases, and reconciliation actions happen across teams and internal systems, businesses need a reliable record of who did what, when, and why. This is essential not only for compliance but for understanding the history of a transaction when something goes wrong.

These problems are deeply operational but also architectural.

If the internal system of record is weak, teams cannot reconcile external events cleanly. If the status model is inconsistent, support and finance may interpret the same transaction differently. If workflows are spread across disconnected internal systems and providers, exceptions become expensive to investigate and hard to resolve.

This is why payment infrastructure cannot be evaluated only by how easily it initiates a transaction. It also needs to support the work that happens after the transaction: reconciliation, exception management, cash positioning, approvals, and financial control.

The biggest failures in payment operations often happen when teams lose the ability to answer a simple question: what happened to this money?

What's missing is not another provider within the existing model to execute payments, route transactions, or hold funds.

What's missing is an evolved PSP that can coordinate all these functions, track state across providers, manage workflows for money movement, and maintain a reliable financial record over time.

The next evolution of the PSP

As payment infrastructure expands across more rails, more providers, and more operational dependencies, a pattern emerges.

The challenge is not access to payment infrastructure. It is maintaining a consistent, reliable understanding of how money moves across it.

Across the stack, each provider performs its role:

But no single provider or system of record is responsible for providing a complete and consistent view of what happens across the full lifecycle of money movement.

That's why the next evolution of the PSP is one that provides consistent visibility across the entire stack, so that every payment can be understood, ledgered, and trusted from initiation through final settlement.

Modern Treasury: A PSP for today's full lifecycle of money movement

Through a unified API, Modern Treasury enables businesses to:

Instead of relying on fragmented providers and internal systems to define what happened, businesses can operate from a single, consistent model of money movement.

Getting started with a modern PSP

Modern payment infrastructure is no longer defined by a single processor or a single rail. It is an environment composed of multiple providers, each responsible for a different part of how money moves, is approved, settled, and ledgered.

Throughout this guide, we've seen how that environment evolved.

Payment service providers expanded beyond transaction processing. Payment rails multiplied. Real-time systems removed the safety net of delayed settlement. New forms of infrastructure, including stablecoins, further extended the system.

As a result, the role of the PSP has evolved. Modern payment infrastructure must coordinate workflows across multiple providers, maintain a consistent view of transaction state, and ensure that financial records remain accurate as money moves.

For teams building financial products or embedding payments into software, this requires a different approach to architecture.

A modern payment stack must include not only access to payment rails and providers, but also a layer that manages and explains how those components work together.

That layer must:

Without this layer, complexity compounds as systems scale. With it, businesses can operate money movement with clarity, control, and confidence.

Modern Treasury provides the infrastructure to build and operate with this payment stack through a unified API.

Ready to start building with a modern PSP that will scale with you? Visit Modern Treasury's API Docs to learn more.

Get the latest articles, guides, and insights delivered to your inbox.