Stablecoins For Developers

How to build reliable payment experiences where fiat and stablecoins interoperate.

March 13, 2026

6 minutes

Contents

Modern Treasury connects fiat and stablecoin rails in one API.

Why Developers Should Care About Stablecoins

If you're building or maintaining products that move or store money, you're already dealing with settlement, whether you think about it explicitly or not. Most of fintech innovation has focused on the processing layer: the synchronous part of the formula that lets consumers easily send money to friends or buy something online, and enables businesses to pay vendors and accept bill payments. Under the hood, however, settlement — the process by which money actually moves from one party to another — follows a different set of rules. Traditionally, this has been handled by banks or various flavors of payment processors, built on rails such as ACH or wires, both domestic and international. These systems work, but they weren't designed for a global economy and introduce friction, delays, and costs. Increasingly, stablecoins are becoming a viable settlement layer. They offer developers an alternative way to move value faster, more cheaply, and more efficiently by decoupling settlement from legacy constraints. If you care about efficiency, reliability, and scale in the systems you create, you should care about stablecoins.

Stablecoins are often discussed in the context of crypto trading and speculative investments. But that framing misses another key area where they're gaining meaningful traction: payments and settlement. Today, companies like Visa¹, Stripe², Revolut³, Nubank⁴, and many others are deploying stablecoins as core infrastructure for money movement — enabling instant, more predictable, and more global transactions. They've moved beyond experimentation and into production. Regardless of your company's size, stablecoins can modernize financial systems for everyone, from early-stage startups to global enterprises. This guide isn't about trading, token launches, or crypto-native finance. It explains how stablecoins fit into production payment systems: how they move, where they help, where they fall short, and how developers should design systems that incorporate them safely. You don't need to become a crypto expert to build with stablecoins. But you do need to understand how they change the shape of settlement and what they don't replace.

What are stablecoins?

Stablecoins are best understood as digitized representations of fiat money.

Unlike volatile cryptocurrencies, stablecoins are designed to maintain a stable value, typically pegged 1-to-1 to a sovereign currency such as the U.S. dollar.

From a systems perspective, stablecoins introduce a new money primitive. They function simultaneously as the following:

Rather than living exclusively inside closed banking ledgers, stablecoins move almost instantly across borderless, internet-native networks with transparent state and clear settlement finality.

This architecture decouples money movement from many of the constraints developers have worked around for decades. Stablecoin settlement isn't bound by banking hours, geographic borders, or correspondent banking relationships. Transfers can occur continuously across jurisdictions, without waiting days for reconciliation or confirmation.

Stablecoins are most powerful when they quietly enhance slow or brittle settlement paths behind the scenes, powering use cases such as treasury flows, cross-border payments, platform payouts, and internal liquidity movement without introducing new surface area for users.

Types of stablecoins

While stablecoins are often treated as a single category, there are important structural differences that matter when you're building production systems.

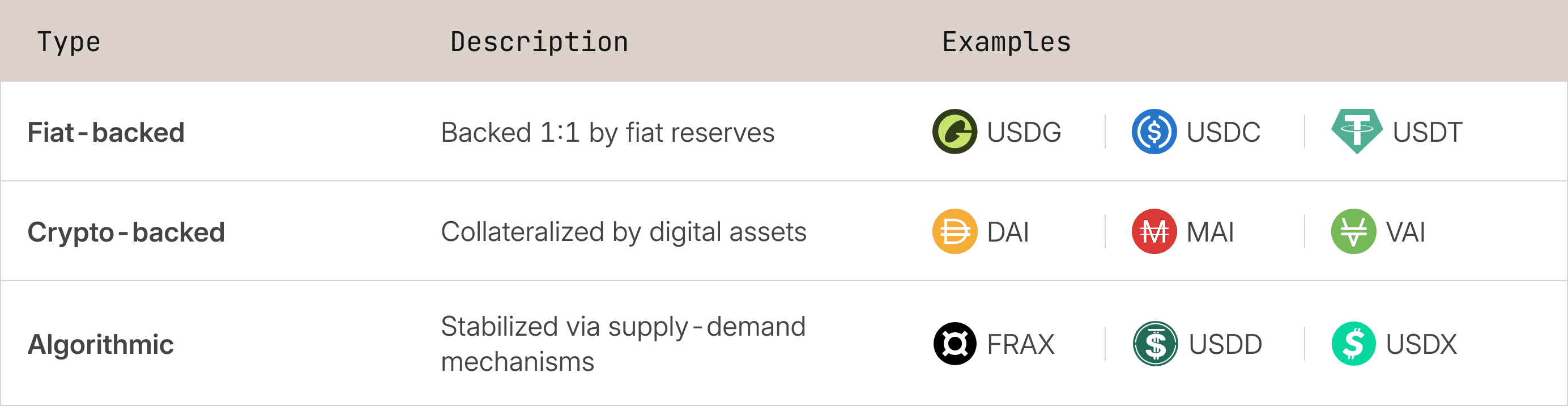

Fiat-backed stablecoins

Fiat-backed stablecoins are the dominant model in real-world usage today. These are issued by centralized entities, backed by cash or cash equivalents, and redeemable 1:1 for fiat currency. Issuers like Paxos (USDP, USDG), Circle (USDC, EURC), and Tether (USDT, USAT) have focused on transparency, reserve management, and regulatory alignment to make these assets attractive to fintechs and infrastructure providers.

There has also been experimentation with non-USD, fiat-denominated stablecoins, including euro-backed tokens such as EURT, pound-denominated stablecoins like GBPT, and yen-linked stablecoins such as GYEN. While these assets demonstrate that stablecoins can technically represent a range of fiat currencies, none have yet achieved the liquidity, distribution, or ecosystem support of USD-denominated stablecoins. As a result, USD stablecoins continue to dominate production use cases.

Crypto-backed stablecoins

Crypto-backed stablecoins rely on over-collateralization with digital assets. While they reduce reliance on traditional banking systems, they introduce market risk, liquidation mechanics, and operational complexity. These properties make them less suitable for regulated or enterprise-grade use cases.

Algorithmic stablecoins

Algorithmic stablecoins attempt to maintain their peg through incentives or supply adjustments rather than explicit backing. While interesting from a research perspective, they have historically proven fragile under stress and are rarely used in serious financial infrastructure.

For developers, stablecoin type affects:

For the purposes of this guide, we will focus on fiat-backed stablecoins.

How stablecoins move

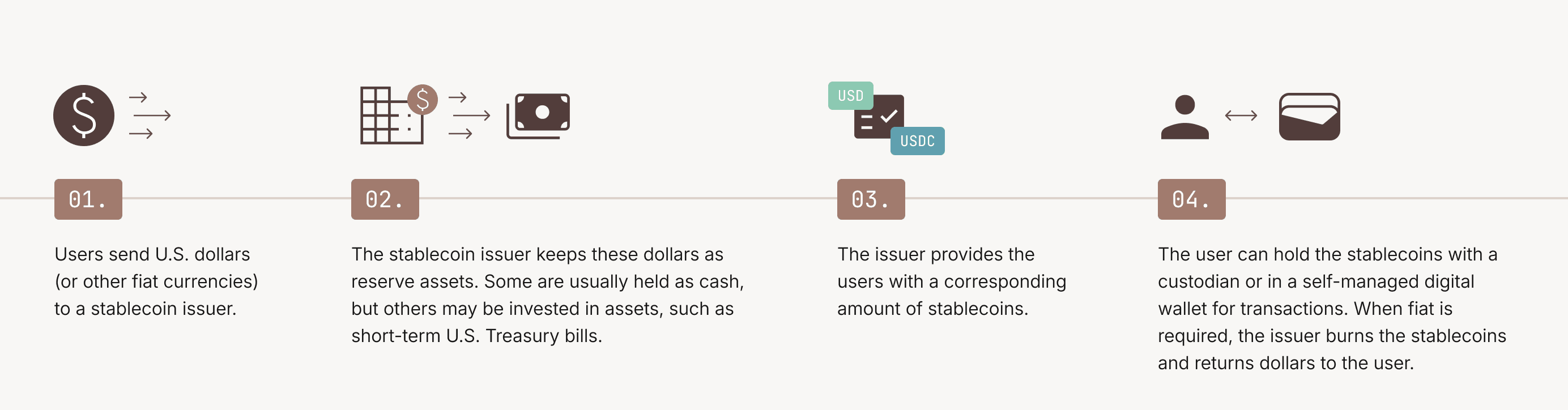

Despite the surrounding complexity, stablecoins follow a simple lifecycle: mint, transfer, and burn. This framing describes the primary market, where stablecoins are issued and redeemed directly with an issuer in exchange for fiat.

In a primary market flow, fiat enters the system through a bank or payment partner and is used to mint stablecoins on a blockchain. Those stablecoins can then be transferred between wallets, effectively on-chain accounts, typically settling in seconds or minutes with clear finality. When holders want to exit to fiat, stablecoins are burned and funds are returned via traditional banking rails.

In practice, much stablecoin activity occurs in secondary markets, where tokens circulate between participants without direct interaction with the issuer. In these cases, stablecoins may move many times on-chain before ever being redeemed, if they're redeemed at all. On-chain transfers are fast, continuous, and transparent. They occur 24/7 without intermediaries and with an explicit settlement state.

Regardless of whether liquidity is sourced directly from the issuer (primary) or from a third party (secondary), the flow between stablecoins and fiat works the same in principle.

This is where much of the complexity lies — at the convergence layer between blockchains and traditional networks. Specifically, in the following areas:

Infrastructure providers such as Modern Treasury focus primarily on making fiat and stablecoin systems interoperable throughout their lifecycles.

Where stablecoins are used in production

Stablecoins are already being used in production systems — just not always visibly. In most cases, they operate as invisible settlement infrastructure, replacing or augmenting legacy rails when speed, cost, or geographic reach becomes a limiting factor. This is evident across a growing range of real-world deployments:

What stablecoins don't solve (yet)

Stablecoins dramatically improve settlement, but they don't solve all financial system problems. They don't eliminate the need for the following:

If anything, stablecoins make these responsibilities more important. On-chain transfers don't inherently handle chargebacks, disputes, or reversals. Liquidity can fragment across issuers and blockchains, and regulatory coverage varies by jurisdiction.

While stablecoins make global settlement faster and more programmable, they haven't yet replaced SWIFT. The limiting factor isn't on-chain transfer, but the ongoing work to build reliable on- and off-ramps across every geography. In addition, stablecoins have yet to fully penetrate the domestic U.S. payments market, given their reliance on entering and exiting payment systems via traditional rails.

In practice, stablecoins are best seen as an improvement to the money movement stack, not a full replacement for it.

Treating them as such leads to systems that are more resilient, auditable, and easier to reason about.

Designing a modern payments stack that's only possible with stablecoins

End users rarely want to use a stablecoin. They want faster payouts, cheaper international transfers, and reliable access to their money.

As a result, most successful implementations hide stablecoins entirely. Companies such as Felix Pago¹³ and Sling Money treat stablecoins as backend infrastructure by exposing familiar account abstractions while using on-chain settlement internally to improve speed and reach. They've processed more than $1 billion in consumer remittances because users want to pay and get paid instantly and with minimal fees, regardless of the rail under the hood.

This mirrors how developers already think about payment rails. Users don't choose between ACH and wires. Instead, systems route transactions based on context. Stablecoins increasingly fit into that same mental model.

Moving between fiat and stablecoins

Any real-world stablecoin system must move value between fiat and on-chain settlement.

This happens through on-ramps (fiat to stablecoins) and off-ramps (stablecoins to fiat). These edges are where the following occur:

- KYC and AML are enforced

- Liquidity is provisioned

- Funds are reconciled with bank accounts

In production systems, ramp reliability matters more than raw speed. Failed conversions, delayed settlements, or limited coverage can break entire flows. This is why teams increasingly rely on orchestration rather than hard-coding a single provider.

The next chapter of stablecoin orchestration

The stablecoin ecosystem is fragmented across issuers, blockchains, and jurisdictions. Developers shouldn't have to pick winners, manage issuer-specific risk, or build bespoke compliance tooling for each integration.

Stablecoin orchestration provides a unifying layer:

This mirrors how modern payment platforms abstract over banks and networks to make complexity manageable without hiding risk.

You still need a ledger

In a perfect world, the blockchain could serve as a platform ledger. In practice, however, the world isn't perfect. Even with significant on-chain settlement, stablecoins don't eliminate the need for an internal ledger when companies interact with fiat, which they all do.

Blockchains record transfers between wallets. They don't capture business logic, user entitlements, pending states, or accounting abstractions. A ledger remains the system of record, tracking balances, enforcing invariants, and enabling reconciliation across fiat and stablecoin rails.

Stablecoins increase the speed of money movement, underscoring the importance of accurate accounting and reconciliation rather than diminishing it.

Getting started with stablecoins

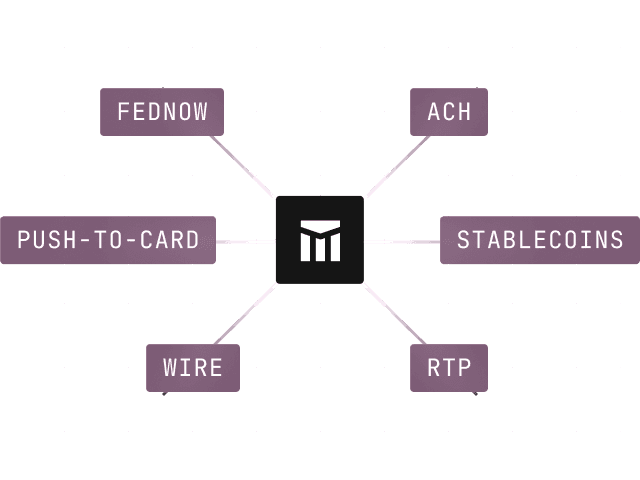

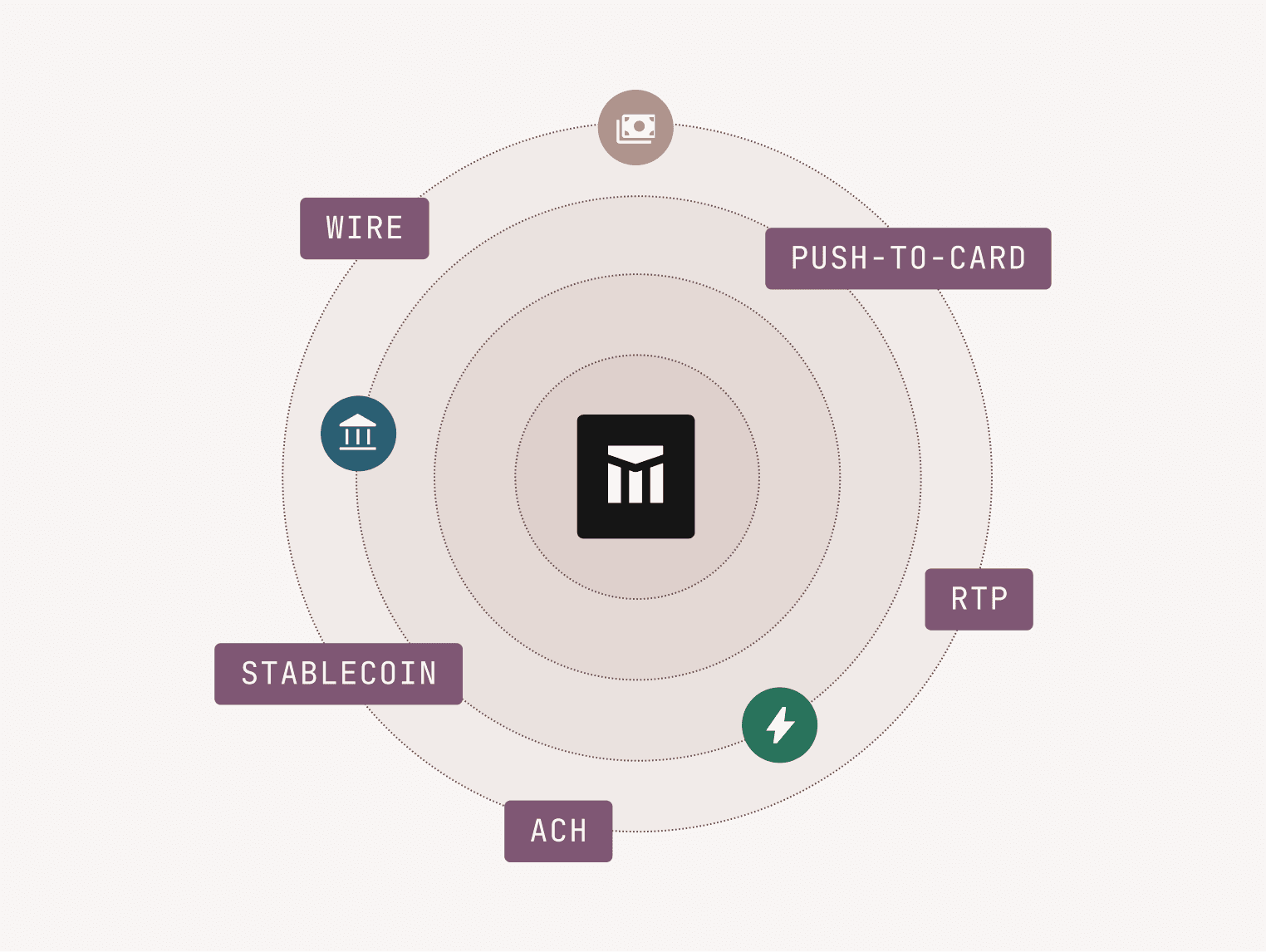

Modern Treasury supports stablecoins alongside ACH, wires, RTP, and other payment rails through a single, unified API.

From a developer's perspective, stablecoins aren't a separate system to integrate or reason about. Instead, they're accessed using the same core primitives used to move fiat.

Most notably, stablecoin flows are enabled using the same primitive as all other money movement: Payment Orders. This means your application logic, reconciliation workflows, and ledger integrations don't need to change simply because you're using stablecoins.

In practice, this allows teams to treat stablecoins as another first-class rail without creating a parallel payments stack.

Stablecoins with Modern Treasury's API

Before diving into specific flows, it's useful to understand how stablecoins appear in the Modern Treasury object model. These core objects include the following:

By reusing these primitives, Modern Treasury ensures that stablecoin settlement fits naturally into existing payment, treasury, and accounting workflows.

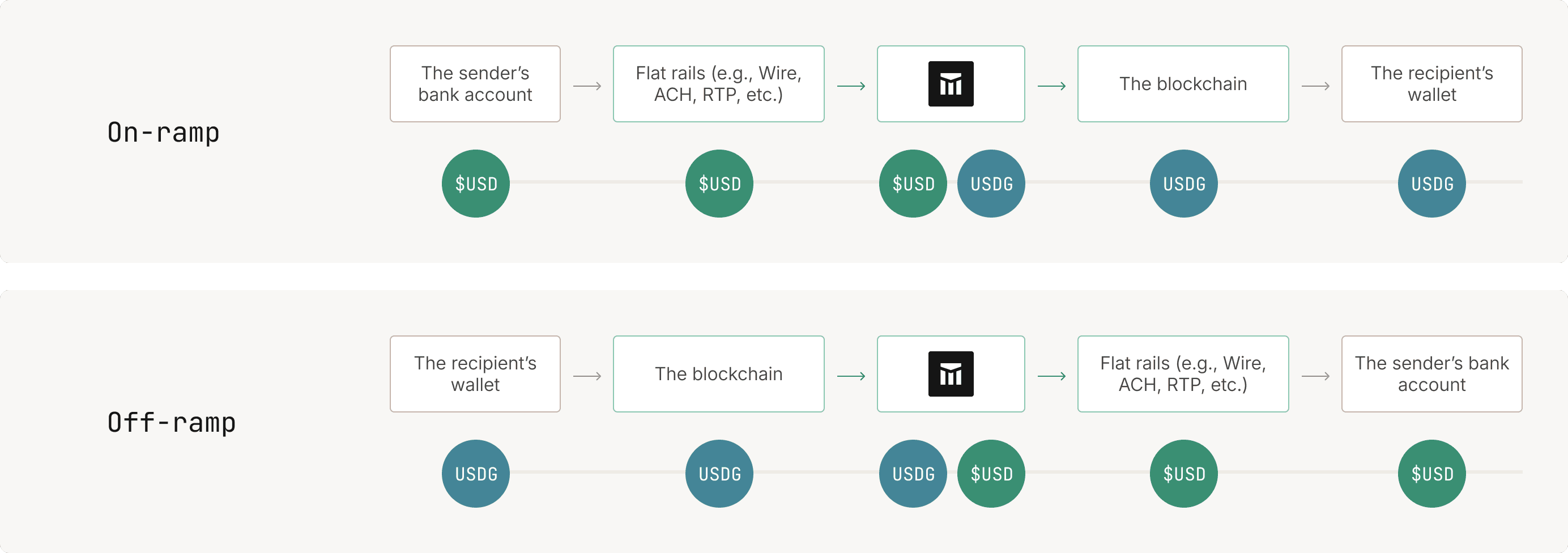

Sending a stablecoin (On-ramp)

An on-ramp flow is used when you want to fund a stablecoin balance and send stablecoins to an external wallet. Common use cases include funding an on-chain savings account, paying a vendor who prefers to receive USDC, or originating payments for on-chain loans or protocols.

In Modern Treasury, on-ramping stablecoins follows the same conceptual model as sending fiat payments, with stablecoins treated as another settlement rail:

01. You fund a stablecoin Internal Account

Stablecoin balances are held in a Modern Treasury–managed stablecoin Internal Account (e.g., USDG, USDC). If you are starting with USD, the stablecoin account is funded via a Book Transfer from a USD Internal Account, representing a USD -> USDC conversion. If the USD account does not yet have sufficient funds, it can be funded using standard fiat rails such as ACH debits, ACH credits, or wires.

02. You Create a Counterparty with a stablecoin wallet address

Stablecoin payments are sent to counterparties defined by blockchain wallet addresses rather than bank account details. Each Counterparty includes an External Account that specifies the destination wallet address, for example, an Ethereum or Solana address.

03. You create a stablecoin Payment Order

To send the funds on-chain, you create a Payment Order with type: stablecoin, using the following:

- Your stablecoin Internal Account as the originating account

- The Counterparty's wallet External Account as the receiving account

Once submitted, the Payment Order follows the same lifecycle as other rails—approval, processing, and settlement—while the underlying transfer is executed on-chain.

04. You track settlement and reconcile the payment

The stablecoin transfer is tracked through Modern Treasury's standard payment status and reconciliation primitives, allowing you to apply the same business logic used for ACH, wires, or RTP payments.

Because stablecoin on-ramps reuse the same Internal Accounts, Counterparties, and Payment Orders as fiat payments, teams can introduce stablecoin payouts without maintaining a stablecoin-only vendor integration or building more complex, lower-level blockchain integrations.

Full implementation details and examples are available in the docs here.

Receiving a stablecoin (Off-ramp)

An off-ramp flow is used to receive stablecoins, convert them into fiat, withdraw funds to an external bank account, and reconcile the activity across your internal records, ledger, and downstream systems.

In Modern Treasury, receiving stablecoins follows the same conceptual model as receiving a wire or ACH credit. The flow includes the following:

01. Stablecoins are sent to a Modern Treasury–managed stablecoin account

This account is associated with your organization and tracks inbound on-chain transfers. Each stablecoin account has a unique address for each supported blockchain that can be used to receive funds from external wallets.

02. Incoming transfers are surfaced as Incoming Payment Details

These objects give you visibility into the following:

- Amount and currency received (e.g., USDC)

- Settlement status

- Timing and identifiers needed for reconciliation.

03. Stablecoins are converted to USD via an internal book transfer

To move from stablecoin settlement to fiat, USDC is transferred from your stablecoin Internal Account to a USD Internal Account using a Book Transfer. This represents the stablecoin-to-USD conversion and keeps the flow fully auditable within your system of record.

04. Fiat funds are sent out on standard rails

Once the USD Internal Account is funded, you initiate a fiat Payment Order (ACH, wire, or RTP) to an external bank account or Counterparty, just as you would for any other USD payout.

05. You reconcile the full flow into your ledger or application logic

This may include crediting a customer balance, marking an invoice as paid, or triggering downstream treasury or payout workflows.

Because incoming stablecoin payments are surfaced through the same reconciliation primitives as fiat payments, teams can apply consistent logic across all rails.

Full implementation details and examples are available in the docs here.

One API, unlimited possibilities

By unifying stablecoins and fiat rails behind the same API, Modern Treasury enables capabilities that are difficult to achieve with most other payment service providers.

This approach lets developers focus on when stablecoins make sense rather than how to wire them up safely.

A future where money moves like data

Stablecoins are becoming first-class rails.

The systems that'll last will treat them as such — pairing them with traditional rails, strong ledgering, and compliance-first design. Stablecoins are no longer a risky bet but a pragmatic upgrade to how settlement works.

The future of money movement is hybrid, programmable, and API-driven. Stablecoins are part of that future because they allow money to move with the same reliability, composability, and clarity as modern software. Providers such as Modern Treasury enable both forward and backward compatibility.

For teams ready to build with the most modern payments software, talk to us.

Sources

¹ Visa Inc. (2025, December 16). Visa launches stablecoin settlement in the United States, marking a breakthrough for stablecoin integration. https://usa.visa.com/about-visa/newsroom/press-releases.releaseId.21951.html ² Fortune. (2025, October 1). Stripe is already a payments colossus. Now it wants to make stablecoins the backbone of global commerce. https://fortune.com/crypto/2025/10/01/stripe-crypto-stablecoins-open-issuance-bridge-blockchain-tempo/ ³ Yahoo Finance. (2026, January 14). Revolut stablecoin payments surge over 150% in 2025: Researcher. https://finance.yahoo.com/news/revolut-stablecoin-payments-surge-over-081837385.html ⁴ CoinMarketCap Academy. (2025, September). Nubank plans stablecoin credit card integration. https://coinmarketcap.com/academy/article/nubank-plans-stablecoin-credit-card-integration ⁵ Fortune. (2025, May 8). Exclusive: Meta in talks to deploy stablecoins three years after giving up on landmark crypto project. https://fortune.com/crypto/2025/05/08/meta-stablecoins-exploration-usdc-circle-diem-libra/ ⁶ Yahoo Finance. (2024, December 21). "SpaceX uses stablecoins to collect payments from Starlink customers," says Chamath Palihapitiya. https://finance.yahoo.com/news/spacex-uses-stablecoins-collect-payments-170027463.html/ ⁷ Klarna. (2025, November 25). Klarna launches KlarnaUSD as stablecoin transactions hit $27 trillion annually. https://www.klarna.com/international/press/klarna-launches-klarnausd-as-stablecoin-transactions-hit-usd27-trillion/ ⁸ Finovate. (2026, January 20). Gusto unveils global stablecoin payout capabilities. https://finovate.com/gusto-unveils-global-stablecoin-payout-capabilities/⁹ Reuters. (2024, July 24). Ferrari extends cryptocurrency payment system to Europe after US launch. https://www.reuters.com/technology/ferrari-extends-cryptocurrency-payment-system-europe-after-us-launch-2024-07-24/ ¹⁰ The Defiant. (2025, August 5). Californian neobank Slash bets on own stablecoin to streamline global dollar access. https://thedefiant.io/news/tradfi-and-fintech/californian-neobank-slash-bets-on-own-stablecoin-to-streamline-global-dollar-access ¹¹ American Banker. (2026, January 29). Neobank Dakota launches stablecoin platform for businesses. https://www.americanbanker.com/payments/news/neobank-dakota-launches-stablecoin-platform-for-businesses ¹² TechCrunch. (2022, September 14). Kaszek, YC back DolarApp's mission to 'dollarize' Latin America's finances with crypto. https://techcrunch.com/2022/09/14/kaszek-yc-dolarapp-latin-america-crypto/ ¹³ Stripe. (2025, August). Félix powers $3 billion in payment volume through stablecoins and AI-driven remittances. https://stripe.com/customers/felix

Get the latest articles, guides, and insights delivered to your inbox.