Announcing Our First $100M Month

Today, we are excited to announce that Modern Treasury reconciled over $100 million in payments for our customers last month. This milestone comes after compound monthly growth of 25% since January.

Explore With AI

Today, we are excited to announce that Modern Treasury reconciled over $100 million in payments for our customers last month. This milestone comes after compound monthly growth of 25% since January.

Building infrastructure takes time. On our YC demo day, we weren’t yet live because we were still completing our first bank integration. Our first customer signed at the end of that year, and our first ten customers took another nine months. After years of engineering and product investment in a first-of-its-kind payment operations platform, it feels good to see so many teams use what we built every day.

Our vision is that reconciliation should be instant, anytime, all the time. Our platform enables engineering and finance teams to innovate while taking control of their financial processes. Gone are the days of messy CSVs, outdated bank portals, and rushing to click release before an approval window closes. Our system handles all of that automatically. We believe software should not just initiate, but also monitor and reconcile payment activity.

By value, over 92% of noncash payments occur over ACH and paper check [1] and have a four part cycle: initiation, approvals and release, reconciliation, and accounting. To measure how much value we’re providing to engineering and accounting teams, we use dollars reconciled as our north star metric. [2]

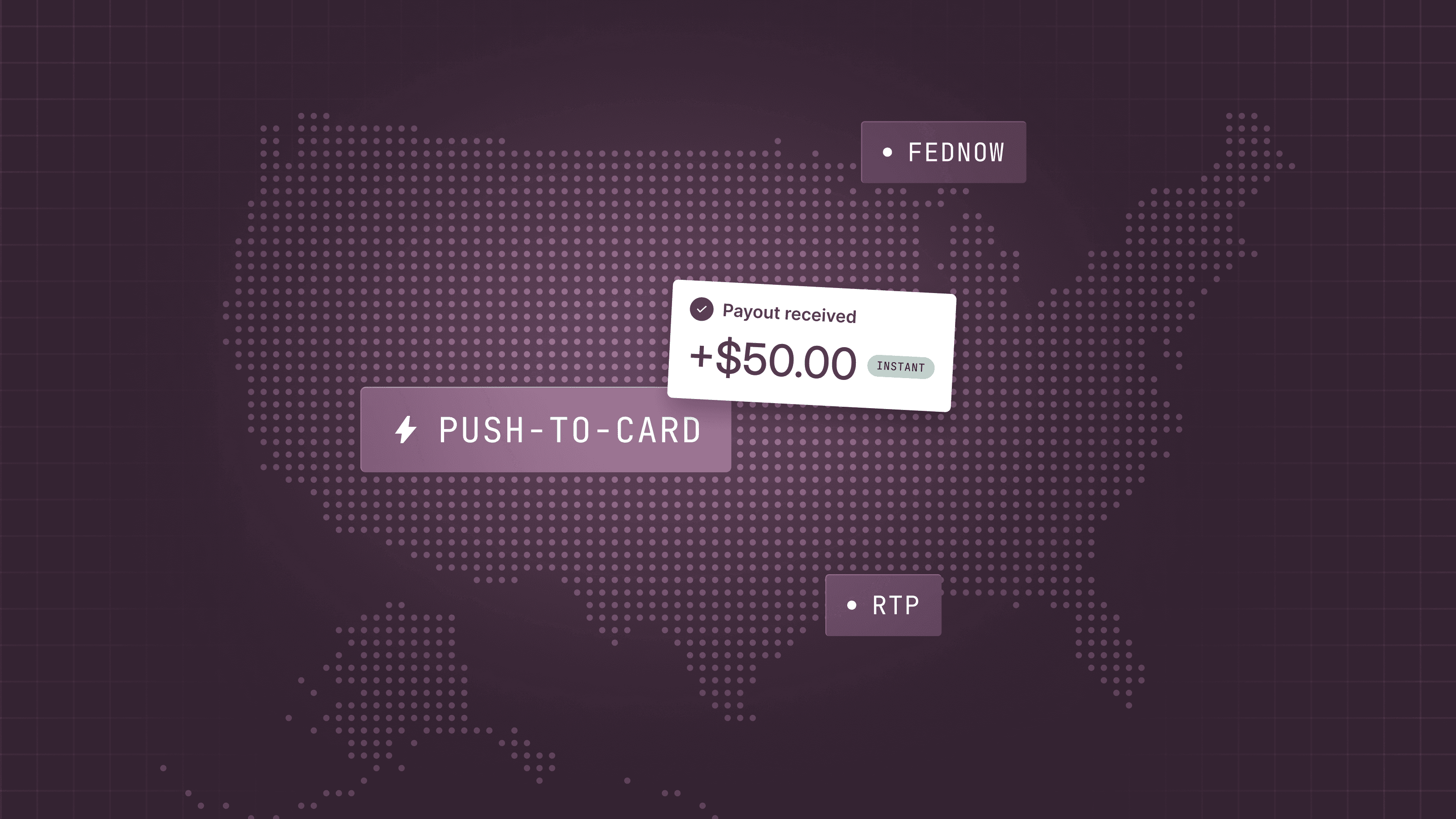

We are especially proud to have helped initiate and reconcile over $5M in Real-Time Payments (RTP) last month. With RTP, our customers can offer instant, 24x7x365 payouts. And as payments become real-time, the pressure on payment operations, control processes, and month close is mounting.

To put RTP into historical perspective, it is the first payment rail introduced in the United States since ACH appeared in 1974. That was the year Nixon resigned and Gerald Ford became president and the top songs were Waterloo and Dancing Machine and Subarus looked like this. Payment platform shifts do not happen often. With this new technology, we have a chance to unlock 3 days' worth of the American economy that is tied up in ACH settlement purgatory.

Thank you to all our customers who constantly inspire us, ideate on products with us, and send us great Slack emojis. Reach out if you’d like to learn more about the product or to join the team. We’re hiring!

What is past is prologue, and we’re just getting started with Chapter One.

Get the latest articles, guides, and insights delivered to your inbox.

Authors

Dimitri Dadiomov is the co-founder and President of Modern Treasury. Dimitri started his career in product and business development at Better Place and then moved to venture capital before earning his MBA at Harvard Business School. Dimitri is a graduate of Stanford University and spends his free time skiing, hiking, writing, and devouring books.