How Financial Decision Makers Deal with Marketplace Payments

Learn how marketplace payments happen today—the practices and issues, associated losses, and what leaders want for the future.

Modern Treasury recently surveyed 500+ financial decision makers and released, in partnership with The Harris Poll, our third annual State of Payment Operations Report. From product and treasury teams to marketplace payments leaders, data revealed a host of challenges around money movement, amplified by manual inefficiencies, bloated tech stacks, and in-house builds.

"There's a lot of pain in business payments," Rachel Pike, Modern Treasury’s COO recently told American Banker. "But we think things are changing; I'm seeing a lot more self awareness among businesses that payments need to improve."

According to report data, companies that describe themselves as marketplaces displayed a particular awareness of problems related to payment operations and infrastructure, coupled with a marked desire for change. This article explores current marketplace practices and issues, resulting business losses, and what leaders want for the future.

The Present (Painful) State of Marketplace Payments

Overall, decision makers shared that over one-third of their payment operations are manual. For marketplace payments in particular, this ratio is closer to two-fifths (38% reported). This figure includes processes like making payments, tracking payment status, reconciling payments, and monitoring cash balances.

Nearly one-third of marketplaces are toggling between tools to oversee money movement. 32% of marketplaces use five or more systems to manage payments and 18% use between five and nine systems.

Marketplace leaders also reported that the largest portion of their payments are made by way of a third-party tool, such as a payments platform or third-party tool. This is distinct from survey respondents as a whole, who made the largest portion of payments online via bank portal.

Given this reliance on third parties, it’s not surprising that 86% of marketplaces reported using a third-party provider—a five percentage point lead above usage reported by decision makers across verticals.

Dependence on third-party providers can not only limit financial control but also extend processing times. Perhaps for this reason, marketplaces reported a higher incidence of payment delays than respondents as a whole in every category, with a difference of up to six percentage points.

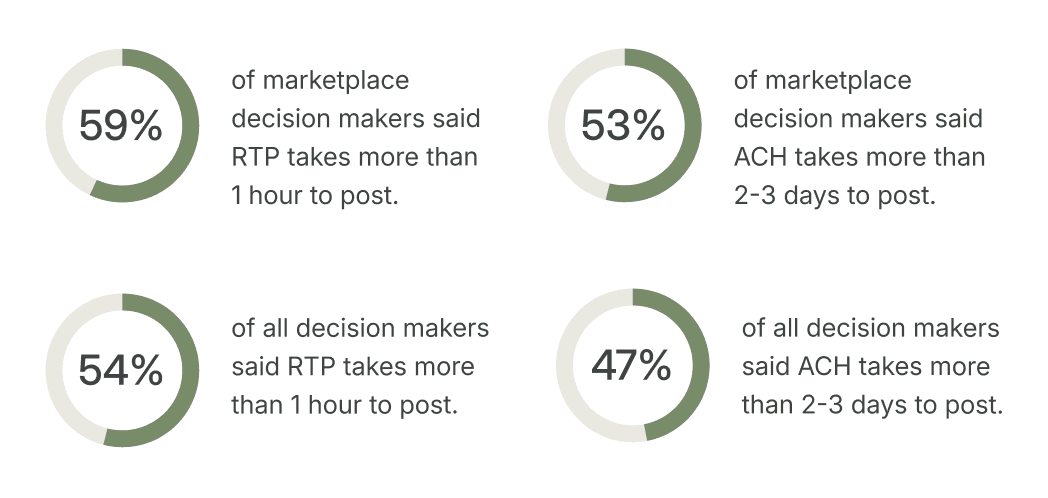

As an example, 59% of marketplace decision makers said RTP takes more than one hour to post (vs. 54% of all leaders who reported the same); 53% of leaders from marketplaces reported that ACH takes more than two to three days to post (vs. 47% of the whole). Marketplace respondents also reported more delays than all surveyed leaders for same-day ACH, domestic and international wires, and checks.

These delays are especially noteworthy given the importance of speed in marketplace payments. 71% of marketplace leaders reported using instant rails—11 points higher than decision makers as a whole.

Currently, leaders from marketplaces reported using instant rails for remittance and bill payments (79%), as well as payouts and disbursements (78%). In both cases, the benefit of instant rails is likely being offset by lags in settlement.

Banks matter for marketplace payments—99% of marketplace leaders said that bank rails are important, vs. 97% across surveyed leaders. Marketplaces are also more likely to have built their own integrations—69% reported building in-house vs. 59% of respondents as a whole.

Negative Impacts

In light of these data points (especially around manual work, third-party tools, delays, and proprietary builds), it follows that marketplace decision makers were more likely to describe their payment operations in negative terms. 40% said payment operations were complicated (vs. 37% of all leaders who chose this term)—they also described payment operations as inefficient (34% vs. 28% reported by all respondents) and unsecure (21% vs. 16%).

Over half of marketplace leaders described their payment operations as stressful (51%). Again, reported challenges support this sentiment.

Marketplace decision makers reported higher incidences of payment failures—34% said that more than 10% of payments fail (vs. 29% reported by all respondents) and 26% said that 11-20% fail (vs. 24%).

Marketplaces also seem to experience more problems with reconciliation. 28% of decision makers reported a low rate of accurate payment reconciliation (five points above the percent reported by all decision makers) and 53% said that less than 80% of payments are accurately reconciled to their bank statement—for all leaders, 46% reported the same challenge.

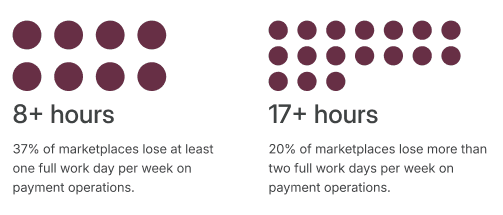

One net result of payment difficulties is valuable time lost for marketplaces. 70% of leaders reported that managing marketplace payments takes too long from start to finish.

Over one-third said they lost more than 8 hours per week (37%) and 20% said they lose over 17 hours per week (four percentage points higher than the norm).

Marketplace decision makers were more likely to report that their finance team wastes a lot of time on payment operations (66% vs. 64% reported by all respondents) and that it’s hard to get a complete financial overview of money movement across multiple bank accounts (71% vs. 67% across all surveyed leaders).

The Desired Future State for Marketplaces

Marketplace decision makers indicated a clear motivation to address challenges around money movement (and curtail associated losses). 97% said that improving payment operations is a priority vs. 92% of survey respondents as a whole.

96% of marketplace leaders said they were likely to invest in payment operations within the next 12-18 months—three percentage points more than what leaders as a whole reported.

They also show greater responsiveness to market conditions. These leaders were eight percentage points more likely to say that, in light of the current economy and stock market, plans to invest in payment operations have sped up (63% vs. 55%).

Marketplace leaders anticipate substantial gains from improved payment operations.

100% of decisions at marketplaces said that upgrades to payment operations would be helpful.

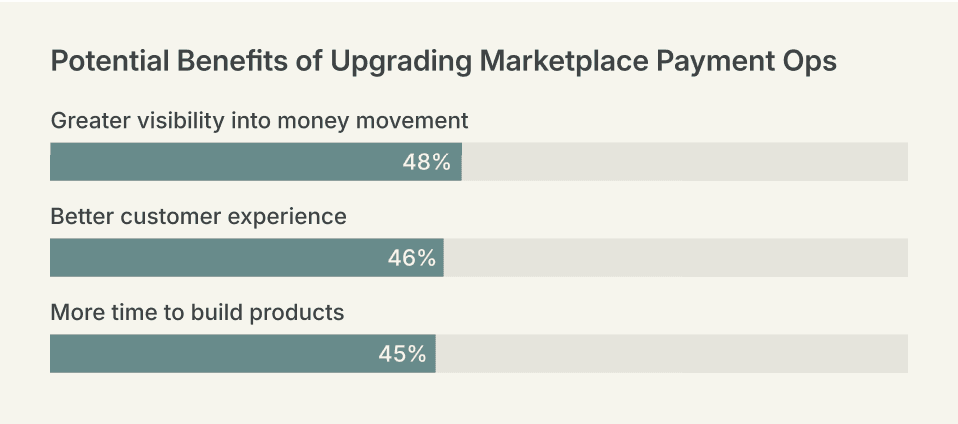

Among potential benefits, these leaders identified the ability to gain more visibility into money movement as most important (selected by 48% of marketplace respondents). In order of importance, marketplace decision makers also identified better customer experience (46%) and more time to build products (45%) as significant desired benefits.

While they were more likely to indicate that improved payment operations are important, marketplace leaders were also more likely to report impediments to change. 92% (vs. 90% of all respondents) said they face barriers to upgrading their company’s payment operations. The primary barrier? Lack of resources from the technical team, as reported by 41% of marketplace decision makers.

The Road to Modern Marketplace Payments

Modern Treasury was founded to provide the technical resources businesses moving money require—especially marketplaces for which scale relies on automated, seamless, and secure payments.

For this reason, our solution is trusted by notable companies like ClassPass and Outdoorsy for marketplace payments. Using Modern Treasury enables seamless back-office payment operations, given a robust API and strong controls that improve efficiency for both engineers and finance team members.

If your marketplace is looking to speed up and simplify payments, or you simply need help navigating this new era of payments, .

About 255 respondents were from companies they described as “a digital peer-to-peer marketplace (i.e., Airbnb, Uber, Upwork)” that span various verticals; data includes their responses as well as non-digital, e-commerce, and company specific marketplaces.

Payment Operations