Digital Payment Platforms are Transforming Payment Operations

Learn how digital payment platforms like Sana Benefits are transforming payment operations.

Health insurance companies typically employ squadrons of finance staffers to collect and manage monthly premiums from across their customer base. But not Sana Benefits, a tech-driven firm based in Austin, Texas, and long-time customer of Modern Treasury.

The company’s digital payment platform automatically collects the premiums from the bank accounts of the nearly 2,000 small and medium-sized businesses it serves. And this automation translates into real cost savings.

“We have a very small team that manages payments, as opposed to an army of people trying to run down monthly payments,” says Paul Dreyer, Sana’s VP of Finance.

Digital Transformation is Coming for Finance

Payment operations are ripe for transformation. For those in finance willing to embrace today’s modern, cloud-based platforms, the payoff is all but guaranteed, in everything from efficiency to the ability to benefit from changes that are sweeping the industry.

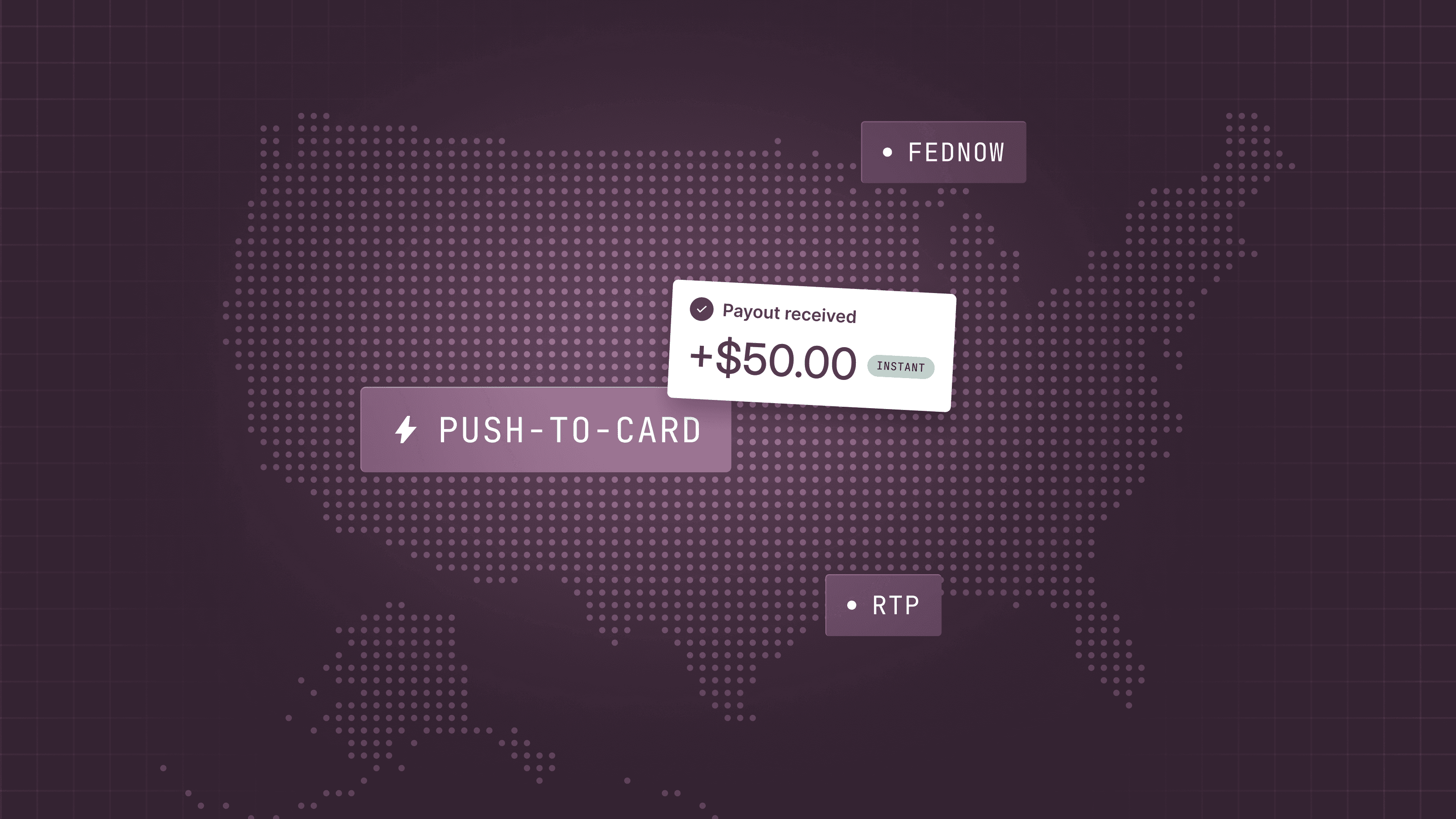

One such big change on the horizon: Later this year, the Federal Reserve Iaunches FedNow, a new payment rail that will send and settle transactions instantly. Another breakthrough: data-handling capabilities for reconciliation “that allow for real machine-to-machine communications,” says Justin Pituch of Glenbrook Partners, a San Francisco–based payments consulting firm.

“If you’re not thinking about different ways for handling your payments in a more timely fashion, you’re not really managing your cash,” says Elena Whisler, a senior vice president at The Clearing House, a consortium of the country’s largest banks. “Today’s CFOs need to be aware of the options they have today so they can plan for it.”

Yet finance departments have not always embraced digital transformation, Whisler and others say. While top finance leaders agree in survey after survey that digital transformation is a top priority, when it comes to payment operations, the needs of finance departments are often an afterthought.

For those resisting change, the costs will only increase, as the seismic shifts that have redefined so many other aspects of today’s business world are quickly remaking payment operations.

“Change is coming whether CFOs are ready or not,” says Dimitri Dadiomov, co-founder and CEO of Modern Treasury.

Eliminating Manual Work

The old days of payments between businesses meant a paper check sent through the mail coupled with an invoice explaining what it was for. Since the 1970s, the Automated Clearing House, or ACH payments, allowed businesses to replace the physical check with electronic transactions.

But ACH has its shortcomings: transactions often take one to three business days to settle, with limited data about the transaction. As a result, using ACH, Pituch says, “in most cases, means emailing somebody a PDF of a remittance document. That creates all sorts of manual work where somebody has to say, ‘We received this ACH payment, now let’s line it up with this remittance document.’”

Another big change in payments hit at the end of 2017, when The Clearing House debuted Real-Time Payments, or RTP. And later this year the Fed launches its real-time payments platform, FedNow. Like RTP, FedNow will move money within seconds, no matter when a payment is initiated. And both RTP and FedNow payments will be enriched with data that is delivered to banks in a standardized format.

“What's really exciting is by natively building in those data-handling capabilities into the payment itself, businesses can get away from situations where staff has to line up invoices, purchases and remittance information,” Pituch said. “Messages can be generated by a financial software tool and then ingested by another financial software tool without human intervention.”

Lowering Costs, With Better Intelligence, At Scale

But modernizing payment operations—which has emerged as the catch-all phrase for the processes and tools that facilitate a company’s money movement, from initiating and receiving payments to resolving problems and reconciling transactions with bank statements—is about more than speed. Those who’ve embraced modernization have reaped benefits that range from lower costs to greater intelligence, superior scaling and real-time tracking of a company’s true financial picture.

The story of Sana, which built its finance operations on Modern Treasury, is a case in point. “We’ve been able to run our business with a very lean team and bypass a lot of the headaches and costs of dealing with manual processes,” says Dreyer.

“Finance software is just kind of stuck in a previous era in terms of tracking everything,” Dreyer adds. “Like what’s my balance? How does this transaction tie back to payment orders created? But we have a better operating system for our financial operations.” That translates into easier onboarding of every new business customer and a clearer, more up-to-date snapshot of Sana’s finances.

Glenbrook’s Pituch says modernization of payment operations often makes the most difference for enterprises that handle large volumes of financial transactions across multiple banks. Faster payments mean a company typically has more time to initiate a payment, since its counterparty will receive it almost immediately.

“There’s advantage both in receiving faster and delaying sending, especially in today’s environment of rising interest rates, where working capital is more expensive,” he says.

Even more savings derive from automation, Pituch says. Moving from manual processes means CFOs can cut the costs of their own operations while taking advantage of the data generated once machines are communicating autonomously with every transaction.

“What’s really exciting for me is the data-handling capabilities of the payment itself,” he said. Companies can improve their forecasting and derive any number of other benefits using analytics and machine learning. “You have all this rich, formatted data to help with every aspect of your operations,” Pituch says.

Additionally, clarity into an organization’s finances can be a powerful weapon for any leadership team seeking to make decisions in a fast-paced environment. “Faster payments help with better visibility,” Pituch says. “That gives you a more accurate picture of how much money you actually have at any given time.” And knowing where your money is translates into better financial decision-making.

An Autonomous Future

Sweeping technological changes invariably require an organization to rethink some processes and create new ones, and payment operations are no different. Company systems will need to operate in a 24/7 environment and meet the demands of both internal users and customers.

“To be ready for real-time payments, an organization not only has to change its [finance] applications but its processes and their oversight,” says Whisler of The Clearing House, which works with the nearly 300 banks (out of some 3,000 nationwide) that use its RTP product. Instant payment can’t be undone when the money moves faster than a human can stop a transfer of funds. Controls need to be strengthened on the front end of a transaction. “A company’s risk profile needs to be adjusted,” Whisler says.

Yet while there are risks inherent in sticking with the legacy systems in use today, there are also risks that will come with failing to act. “We’re at this inflection where a lot of things in the world are speeding up, especially around payments,” Modern Treasury’s Dadiomov says. Those companies that don’t start preparing now for this future are the ones that will miss out.

Get the latest articles, guides, and insights delivered to your inbox.

Authors

Chris Frakes is the Head of Content, Brand Marketing, and Communications at Modern Treasury. She likes to write and edit pieces that help demystify complex products. She's formerly a journalist, banker, and consultant, and has over a decade of experience in fintech.