A Complete Primer on FedNow

Read our eBook to discover everything you need to know about FedNow—from launch plans and use cases to costs and benefits.

July 1, 2023

25 minutes

Contents

The Impact of FedNow

Designed by the Federal Reserve, FedNow will be the first new payment rail in the United States since the introduction of the Automated Clearing House (ACH) in the early 1970s. FedNow enables faster bank payments for financial institutions of any size, in any community, 365 days of the year. The Federal Reserve has announced a release date of July 2023.

While services like PayPal and Venmo are already revolutionizing the world of instant, person-to-person payments, FedNow's mission is to increase accessibility, efficiency, and widespread adoption of faster payments. The FedNow service will incorporate clearing functionality into the process of settling each payment, meaning that financial institutions will be able to instantly exchange the necessary information to debit and credit customer accounts. As a result, banks will also be able to notify customers of completed or failed payments faster.

Similar to RTP, the FedNow service enables instant fund transfers between two bank accounts, even on bank holidays, weekends, or outside of business hours. What sets FedNow apart from RTP and other instant payment services is that FedNow will service all federal reserve banks through the FedLine® network, which provides payment and information services to over 10,000 financial institutions. Once launched, the initial transaction limit for FedNow will be $100,000.

Currently, hundreds of different banks and payment processors are taking part in FedNow's pilot program. The hope is that widespread adoption of the FedNow service, specifically by smaller regional banks, will make instant payments more accessible to the general public in the years to come.

How Much Does FedNow Cost?

In early 2022, the Federal Reserve released pricing and fee details for their real-time settlement network. Because FedNow is government-operated, it's mandated to break even and not turn a profit. A possible advantage of this is that FedNow may offer more competitive pricing than other payment systems, which could encourage widespread adoption at a faster rate.

The anticipated fees include:

- A $25 monthly participation fee for each routing transit number (RTN) that receives credit transfers.

- A $0.045 per credit transfer fee that is paid by the sender, including returns.

- A $0.01 fee for a request for payment (RfP) message that requestors must pay. This includes both new payment messages and returns.

The Federal Reserve will evaluate the credit transfer limit on an ongoing basis and adjust as appropriate.

What Are the Benefits of the FedNow Service?

One of the biggest benefits of FedNow is that it offers support to more financial institutions, including smaller, community banks. While RTP is equally efficient, it is not ubiquitous; it is currently supported by select banks in the U.S. Many banks and non-bank payment services like Venmo and Paypal already offer instant payments or transfers through the RTP networks, but often at an additional fee. FedNow is designed to open up instant payment services to more banks.

The Fed noted that they are, "uniquely positioned to build an instant payment infrastructure, given [their] long history of operating payment systems to promote a safe, efficient, and broadly accessible payment infrastructure."

As FedNow adoption grows, more people can benefit from instant payments. Businesses can operate more efficiently with instant settlements, knowing exactly how much they have in their budget at any given time. This is also ideal for individuals who can access their paycheck faster. When sending money is cheaper and settling is faster, both businesses and individuals benefit.

Business benefits include better efficiency, fewer errors, and increased customer convenience. In addition to back office benefits afforded by fast, non-reversible availability of funds, FedNow could help teams in B2B scenarios (especially those in A/P and A/R) correctly track and post incoming funds (and thus avoid having to reverse errors). FedNow could also be a boon for customers who may need to closely manage outgoing funds. In the case of B2C, instant payments could radically transform the spending (and lives) of customers, especially those living paycheck to paycheck.

The first release of FedNow will also include some optional features, including fraud prevention tools, QR codes, the ability to join initially as a receive-only participant, requests for payment capability, and tools to support participants in their handling of payment inquiries.

Use Cases for FedNow

FedNow has been built to potentially serve a number of business, consumer, and government use cases. For businesses, FedNow can streamline payments to customers, consumers, and employees, as well as speed up B2B transactions.

For consumers, faster payments like FedNow will be a solution for sending funds between accounts, paying friends and family, paying bills, and more. And the government's use of FedNow could radically alter the financial landscape of the United States—tax returns, as an example, could be processed in record time.

What Are the Business Use Cases for FedNow?

In the coming years, businesses will be able leverage FedNow for B2B and B2C transactions.

Business-to-Business (B2B) Payments can be a game-changer in maximizing access to capital for businesses, especially via Requests for Payments (RFP) (or other e-invoices). RFPs that will allow businesses to bill customers directly and the customer can approve and send payment from their banking app in one step.

Business-to-Consumer (B2C) Payments via FedNow will potentially have immense personal value for consumers and end-users. As an example, while claimants currently need insurance claim payouts fast, those payments are usually made via paper check (plus insurance payouts can take up to 70 days or even an unspecified amount of "reasonable time"). The use of FedNow for insurance disbursements would dramatically improve access to funds for those who need them quickly.

Per a recent survey from the Federal Reserve, more businesses see the utility of faster payment rails like FedNow. Interest spans companies of all sizes and is present across use cases.

For B2B and B2C payments, businesses will also want to make sure that they have a ledgering system set up to handle and track FedNow payments. Since faster payments are immediate, companies can't wait to record and reconcile those transactions. Thorough, well-running Know-Your-Customer (KYC) and Anti-Money Laundering (AML) policies are also a necessity.

What are the Consumer Use Cases for Faster Payments?

For consumers, faster payments offer instantaneous solutions for sending funds between accounts, paying friends and family, paying bills, and more. Let's look at a few examples.

Account-to-Account (A2A) Payments allow for the transfer of funds from one account to another, typically between accounts owned by the same customer. Historically, you might have to write yourself a check to move money from one of your bank accounts to another or from a checking account to a brokerage account, for example. With faster A2A payments, that process is streamlined and removes the need for a check.

Peer-to-Peer (P2P) Payments are probably the most ubiquitous of the faster payment options—with consumers being able to electronically send money using services such as Venmo, Paypal, Zelle, or CashApp. P2P payments are useful for paying for services—like babysitting or dog-walking—or for paying friends and family. P2P payments can make something like splitting the check for a meal with friends straightforward.

Consumer-to-Business (C2B) Payments occur when consumers pay a business for their goods and/or services. C2B payments are also useful for making bill payments—imagine paying your cell phone, electricity, and water bills all instantly, rather than mailing a check or waiting several days for an ACH payment to clear. C2B faster payments can also help consumers avoid late fees on payments, because they can be confident that their payment posts to the biller's account right away.

Government Use Cases for Faster Payments

Government-to-Consumer (G2C) Payments have the potential to vastly change the financial landscape of the United States. Something as routine as getting a tax return could be sped up significantly. Once your yearly taxes are received by the IRS, they could issue your tax return and it would hit your bank account the same day.

Instant G2C payments could also be utilized in times of crisis or disaster. Currently Federal Emergency Management Agency (FEMA) applications for assistance can take up to 10 days to be received and processed. It then takes at least another 10 days to receive a FEMA disaster relief payment, if your application for assistance is approved. That payment sometimes comes via check, meaning affected people then need to either go to a bank to deposit it or go to a check cashing facility. The whole process can involve 20+ days of waiting for funds. Instead, faster payments technology could help get money into the pockets of affected people right away.

Consumer-to-Government (C2G) payments are also an honorable mention here: imagine paying taxes, paying to renew a driver's license, or paying application fees for a local permit instantly.

How FedNow Works

A "faster payment" like FedNow is characterized by three qualities: instant transaction settlement, 24/7/365 availability, and immediate confirmation of the payment for both sender and recipient.

Faster payments can operate in either "closed loop" or "open loop" systems.

Closed loop systems process transactions through a single provider, and both sender and receiver are required to have an account with that provider in order to complete payments. Examples of closed loop systems include apps like Venmo, Cash App, and Paypal, where sending funds from one person to another is quick and simple. However, transferring funds out of the app itself can take 24 hours or more as the funds have to then move from the app to the payee's account at a bank, which is outside of the "closed loop."

Open loop systems enable transactions between accounts at different banks and don't require participants to hold an account with a specific app or financial institution. Open loop payments are made via a shared network—like the RTP Network, Zelle, and FedNow—that routes and settles payments for any financial institutions enrolled in that network.

How Is FedNow Different From ACH (and Other Traditional Payment Rails)?

Faster payments like FedNow require rails that are distinct from traditional bank rails like ACH in three primary ways.

1. Processing (Batch vs. Transaction)

Traditional rails use batch processing for ACH, meaning relevant FIs compile and batch ACH transactions before sending them to a clearing house in bulk. Because of the high volume of ACH payments being processed on a regular basis, batching makes sense.

However, batch processing results in delays. With transaction processing, on the other hand, payment files are processed in real-time, as they come in, on a per transaction basis. This dramatically increases the speed of money movement; the anatomy of a faster payment like FedNow includes progress through initiation, authorization, transmission, acceptance, and receipt at a nearly instant clip, payment by payment.

2. Settlement Times

With ACH, clearing via traditional bank rails happens at scheduled intervals. For faster payments like FedNow, clearing occurs transaction by transaction in adherence with ISO 20022—this messaging cadence and an agreement between FIs allows payments to be credited in real-time.

ACH is processed via deferred settlement wherein settlement happens at designated times or on a schedule. FedNow will use real-time settlement; this means settlement will happen on a per transaction basis, at nearly the same time as clearing.

This type of settlement is also called a gross settlement, where FIs clear and settle funds transaction by transaction. For ACH, deferred settlement uses netting (or net settlement), which requires aggregating transactions between the same parties to prevent the depletion of reserves. Real-time gross settlement (planned for FedNow) is much faster with different implications than deferred net settlement related to liquidity and credit risk.

3. Finality vs. Reversibility

Whereas an ACH can be reversed or returned, with faster payment rails, transactions are final, and thus, money is guaranteed. Since the bulk of FedNow payments will likely be credit (or push) payments, there is security that a payer will only be able to initiate payment if they have sufficient funds. This protects businesses from chargebacks on returns like insufficient funds (NSF).

For RFPs, the more robust the data and parameters of the RFP, the less likely errors will be—similar errors in the case of ACH might warrant a reversal. If the amount requested in the RFP, for example, is correctly entered by the payee and can't be edited, mistakes are much less likely. For FedNow, "amount due" will be required as a field in all RFPs.

Understanding Interoperability Between FedNow and Real-Time Payments (RTP)

Though RTP and FedNow have a lot in common—from instant transfers to round-the-clock availability—they are not the same. The Clearing House was heavily consulted while FedNow was being built, and while the two systems work similarly and share some common architecture, they are still two different payment rails.

What Is Interoperability And Why Does It Matter?

Put simply, interoperability is the ability for different software systems to be able to work together via the exchange and use of information. In the context of faster payments, interoperability is the hope that both RTP and FedNow will be able to work in conjunction with one another.

In a recently published comment letter, the American Bankers Association (ABA) asked the Federal Reserve to strive towards achieving technical interoperability with The Clearing House's Real-Time Payments Network. ABA specifically requested that the Fed make changes to include the RTP Network in their proposed revision of Regulation J.

For context, Regulation J "provides the legal framework for depository institutions to collect checks and other items and to settle balances through the Federal Reserve System." The Fed's currently proposed revision to the regulation would create a new subjection applying only to FedNow transactions, with no mention of the RTP Network.

On a more granular level, the challenge around RTP and FedNow interoperability is that, while the communication language that each system uses is the same, the setup for sending and receiving payments via either system is slightly different.

In the US, there are two different types of interoperability: message exchange interoperability and message routing interoperability. With message exchange interoperability you can initiate a payment without the receiving financial institution being on the same service. But for message routing interoperability, both senders and receivers of a payment must be on the same service.

RTP and FedNow won't be inherently interoperable because they only have message routing interoperability. This is confusing because it makes it sound like the two systems will be interoperable, but really it means they're only interoperable with themselves. To send an RTP payment, the receiver will need to be using RTP and vice versa. This is also true for FedNow, both sending and receiving parties will need to be using accounts that are enabled for FedNow transactions.

Where the two systems align as closely as possible is in the messaging specs: both RTP and FedNow will use ISO 20022. ISO 20022 is a standardized way of formatting messages that move money between financial institutions, businesses, and banks. This includes messages with information regarding payments, ATM transactions, fraud, and more. ISO 20022 files facilitate this transfer of information, offering a universal format for domestic and global financial communication.

Every ISO 20022 file has a specific four-part identity, signifying its category, type within that category, variant, and version. These categories are four-character identifiers indicating the message's broad classification, such as cash management, camt; securities clearing, secl; and ATM card transactions, catp.

The standardized use of ISO 20022 could provide FedNow and RTP with a form of message exchange interoperability because messages are sent and received using the same standard.

How Will FedNow And RTP Work Together?

One possible workaround to the issue of interoperability between FedNow and RTP, could be a setup similar to the way FedACH and the Electronic Payments Network (EPN) work together, where both systems are technically separate but interoperate so well that it is difficult to distinguish between the two.

An additional solution could be to look at the way that The Clearing House Interbank Payments System (CHIPS) and Fedwire work together. Together, Fedwire and CHIPS form the primary US network for high-value payments, both domestic and international. Fedwire, as the name suggests, is part of the regulatory body of the Fed and is owned and operated by the twelve Federal Reserve Banks. CHIPS is its private sector counterpart, operated by The Clearing House and owned by the approximately 50 financial institutions that participate in its system.

Fedwire is a real-time gross settlement transfer system, which means that it processes each transaction individually and in full. CHIPS, on the other hand, is a netting engine, meaning the system allows multiple payments between the same parties to be aggregated rather than all processed as individual payments. In 1981, to prevent potential issues from waiting overnight or over a weekend to settle large volumes, the Federal Reserve agreed to provide same-day settlement to CHIPS participants through Fedwire.

Unlike CHIPS and Fedwire, both RTP and FedNow offer the same real-time services, but allowing financial institutions to utilize both could be an answer to the interoperability issue between the two. Because both systems use ISO 20022 messaging format and similar architecture, it is likely there would only be a few differing rules and regulations to manage in sending files between the two. While this sort of arrangement isn't an ideal example of interoperability, it could offer a solution beyond a "one or the other" approach.

Widespread adoption of both FedNow and RTP is likely to be highly dependent on whether or not there is interoperability (or the appearance of interoperability) between the two services. Despite the obvious upsides to FedNow and RTP, if consumers or financial institutions are forced to choose between using either RTP or FedNow, it could be easier to fall back on cheaper, more familiar rails like ACH or card for the majority of payments.

How to Prepare for FedNow

If you're prepping for FedNow—or any other faster payment rail—there are four factors to prioritize during preparation. Spending time on each will make your company's route to quick, smooth payment experiences faster and easier the whole way through.

1. Strategy

To get the greatest advantage from faster payments, invest in research and strategic planning. Your roadmap for faster payments adoption should include the following:

- Understand offerings and opportunities. Each faster payment rail has unique qualities, requirements, limits, and applications. This list of potential use cases for FedNow, as an example, will give you a sense for what is possible.

- Consider alignment with your business goals. Given the faster payments options (including business, commercial, and internal uses), which use cases will you prioritize and how well does adoption match up with higher-level goals?

- Weigh the opportunity costs. Launching and managing faster payments is a commitment that requires both resources and retooling at multiple levels (see below). Will potential gains justify this investment?

2. Partnerships

Without the right bank partnership, your business won't be able to capitalize on faster payments.

At launch, the 12 Reserve Banks and banks in the FedNow Pilot Program will offer FedNow. There are over 120 organizations (banks as well as payment processors and solution providers) in the pilot program, including JP Morgan Chase, Silicon Valley Bank, and Wells Fargo.

If you'll need to partner with a new bank for faster payments, be sure to allow sufficient time for due diligence and onboarding.

Beyond banking relationships, you'll want to consider current partnerships that may be impacted by faster payment adoption—as well as potential partnerships this new technology could benefit from.

3. Technology

Faster payment rails, like any other rail, require technology to support the full cycle of each payment. Necessary capabilities and infrastructure using ISO 20022 include:

- Payment initiation and approvals

- Funds tracking and failure management

- Reconciliation, ledgering, and controls

You may also need to manage counterparties and virtual accounts. Given that faster payments are always on, this infrastructure has to function continuously and autonomously around the clock.

Building an in-house payment operations solution can be complex and costly, especially if you're just standing up a single rail. Modern Treasury estimates, based on client data, that it requires thousands of hours of dev time to create a money movement solution on par with ours.

This data does not account for the need to build a compliance program or ongoing management, maintenance, reliability checks, and improvements—an investment of hundreds of hours per year. It's also likely that breaks and errors will happen outside traditional working hours, putting extra pressure on teams to build (and maintain) diligently.

4. Processes and Tools

Faster payments require upgraded workflows. What works for finance and operation teams handling transactions in batches (daily, weekly, or monthly) won't work for 24×7×365 payments. It's not feasible to staff these roles around the clock—it's also a poor use of team resources.

For offerings like RTP and FedNow, you'll need systems that run around the clock, independently, and even on holidays. And given that over 75% percent of the hours in a week fall outside a standard work day—the most convenient times to complete personal transactions for most consumers—coverage is key.

Faster payments require that you fully automate your entire payments workflow, including the tasks currently done by staff that impact said flow.

As you consider processes affected by faster payments, examine the tools and software in your current tech stack—it may be time to add or consolidate solutions. For a new rail, if you engage a service provider, you'll want to seek out an API-based solution built for end-to-end money movement. If you're already managing multiple rails across banks, it may be time to centralize these workflows within a single platform primed for faster payments.

How To Minimize Faster Payment Fraud

All payments introduce some degree of risk. For most businesses, the benefits of moving money digitally warrant this exposure. Although faster payments rails aren't necessarily riskier than more established rails (including ACH), they are different in three meaningful ways. And each of these distinctions creates new fraud potential for high-growth businesses.

Faster payments are:

- Immediate. Faster payments are built for speed. When money moves instantaneously, fraud can be hard to detect and deter.

- Irrevocable. Faster payments cannot be reversed. Because settlement happens in real-time, fraudulent transactions are nearly impossible to pull back.

- Nonstop. Since faster payments are always on (24×7×365), companies need to be vigilant at all times. Without staffing around the clock, this can be challenging.

Naturally, fraudsters like faster payments just as much as companies and consumers do. When bad actors can move money quickly, leverage instant settlement, and strike at any time, fraud becomes that much more attractive. In response, businesses using faster payments need to establish and solidify safeguards.

It's also important to note the high daily limits for faster payment rails—RTP has a $1 million general transaction value limit and FedNow's credit transfer transaction value limit will begin at $500,000. Clearly, the stakes for understanding and averting potential fraud are sizable.

4 Ways to Minimize Faster Payments Fraud

A key part of faster payments preparation is security. The following suggestions can help companies root out and reduce fraud.

1. Examine risks

To grow a business is to assume some level of risk.

Determining your company's risk tolerance requires balancing the desire for conversions and revenue with the need for compliance and security. For many companies, some degree of fraud is the cost of doing business. PayPal, as an example, at one time purportedly lost up to $1 billion a year to fraud, with a fraud rate between 0.17 and 0.18 percent of revenue.

Fraud prevention must be balanced against friction in the user experience. A recent report found that the average fintech, in an effort to drive growth, loses $51 million to fraud (or 1.7 percent of its revenue) each year, with many losing even more. The report cited the dangerous ripple effect fraud can have, wherein incidents force fintechs to impose barriers that make their customers less likely to move money. This friction—e.g. asking users for more information, algorithms flagging the wrong users, and more manual reviews—can worsen the user experience and thus impact a company's bottom line.

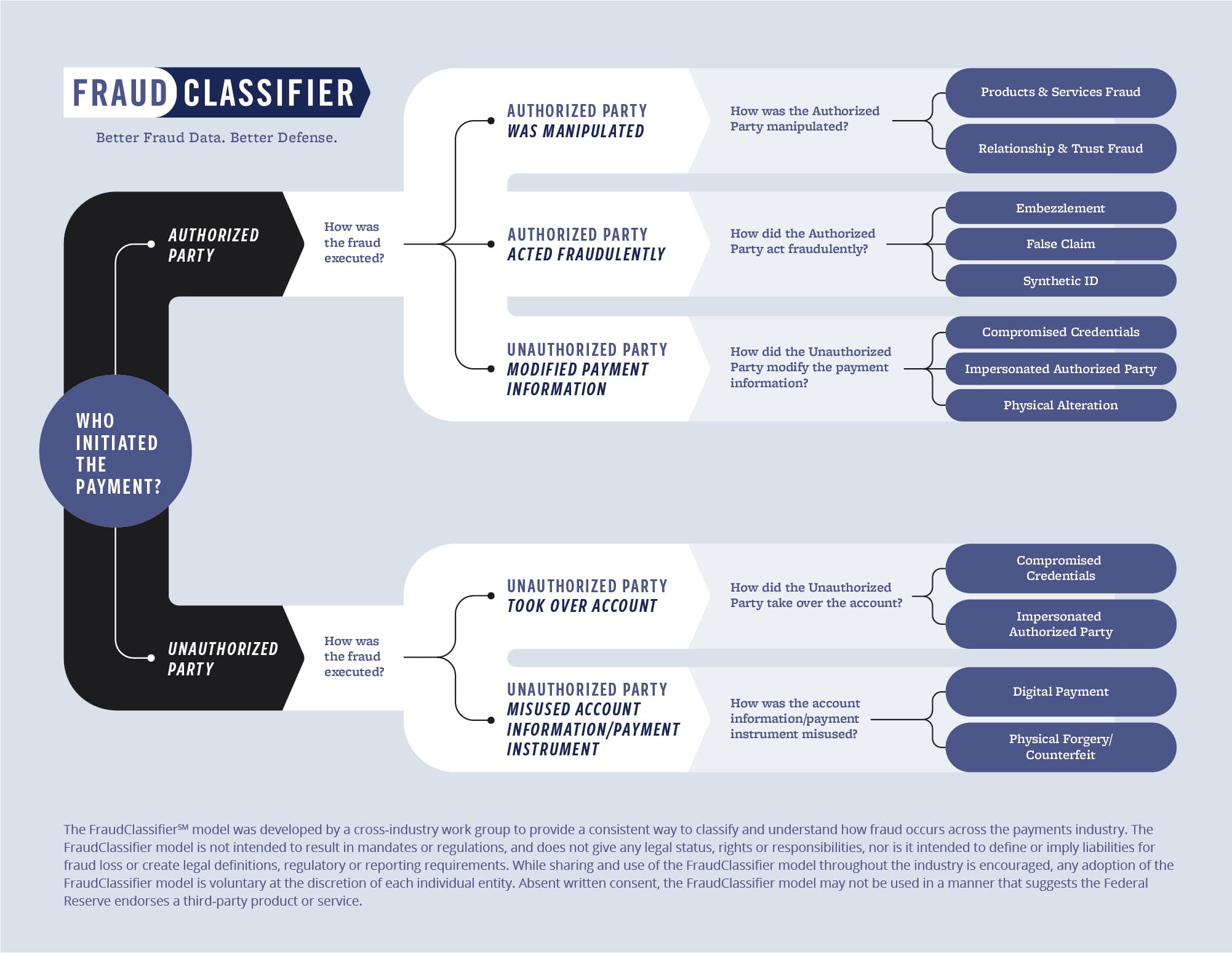

In striking a balance and assessing risk, it's important to understand the different types of payments fraud. The Fed's FraudClassifier Model is a valuable resource for understanding and naming incidents.

As the model shows, fraudulent activity in the payments industry nearly always follows five paths. The type of fraud depends on who initiated the payment (an authorized or unauthorized party) and how the fraud was executed.

- For authorized parties, fraud either involves (1) manipulation, (2) fraudulent actions, or (3) modified payment information.

- For unauthorized parties, the fraudster either (4) takes over an account or (5) misuses account information or a payment instrument.

Different businesses are susceptible to different types of fraud and it is important to consider the risks specific to your business model.

2. Assess tools and processes

When it comes to minimizing faster payments fraud, moving forward requires examining where you currently stand. The following questions can get you started:

- How well do your current tools and processes prevent fraud?

- What adjustments should you make to them?

- Which new tools will you want to add?

- Which processes, across departments, will need to be automated or reimagined to account for payments that are instant, irrevocable, and always-on?

- What process will you use for handling fraud if it arises?

- How will your vendors help mitigate fraud risks?

- What role will your bank partners play in minimizing fraud? See FI requirements for RTP and FedNow.

- Which organizations and communities will help?

Getting a clear understanding of how prepared your business is for faster payments security is crucial. You'll also want to ensure you're using a multi-layered approach to prevent fraud.

A 2022 report breaks fraud prevention into three parts: new account creation, account log in, and distribution of funds. New account creation is the most susceptible to fraud by a wide margin within financial services.

Nevertheless, the incidence and cost of fraud, across all stages, can be scaled back with multi-layered digital identity solutions including email/device verification and behavioral biometrics. In fact, these measures can reduce funds lost to fraud by up to 22%.

Dual approval is another option to consider. This process requires that two authorized users approve a transaction between parties. While dual approval can slow down a payment, the extra time and added oversight can have huge security benefits for certain payment types.

3. Prepare stakeholders

Fraud prevention takes a village. From training team members to educating customers and consumers, reducing fraud requires deep comprehension, buy-in, participation, and diligence.

The Fed advises that business teams be prepared to verify the source of a payment request (e.g., from a supplier or biller). In addition, they should note any changes to payment accounts by using a requestor's known phone number. Educating customers and consumers is also a vital fraud deterrent when it comes to faster payments.

End-users should be encouraged to take precaution. Specifically:

- End-users should be urged to protect personal information like login credentials, ensuring their credentials are strong and unique for each account.

- End-users should be made aware of the irreversibility of faster payments.

- End-users should be informed about their risk for potential fraud and scams.

While FedNow has many advocates, customer security is a concern for some. In the US, the National Consumer Law Center has issued statements indicating that faster payments favor speed and convenience over protection, citing fraud in the UK and via Zelle as model examples.

Still, when companies use the right processes to prepare and educate stakeholders, there's no reason faster payments can't be both instant and safe.

4. Implement and automate security

Circumventing faster payments fraud can be a big undertaking. Companies must be ready to consider a broad array of signals into customer identities and the legitimacy of each transaction. As an example, does the customer pass KYC? Are they using a familiar device and IP address? Are they using a channel and payment type they regularly use?

For many businesses, seeking out the right solution to help is an important part of FedNow readiness.

In choosing the best platform to prevent fraud, be sure to look out for the following features and functionality:

- KYC. Your solution should utilize device and behavior analysis to create a risk score for each new user via multiple data providers (Modern Treasury uses more than a dozen for decisioning, with built in feedback and insights).

- Transaction monitoring. The solution should check for signs of fraud or money laundering, including higher-than-usual payment sizes or volumes, or evidence of structuring behavior. Ongoing checks of customer data are also important, including an updated sanctions screenings, which can catch a user recently added to any watchlists.

- Machine learning and rules engine. User risk levels should be evaluated via machine learning models trained with data from many customers to advance accuracy. A rules engine should also be used for deterministic behavior. Your solution should provide policy controls so that decisions can be automated or manually reviewed depending on risk factors.

Make FedNow a Reality for Your Business

FedNow and other faster payment rails have the potential to radically change the payments landscape in the US. But custom-building a payment operations system ready to handle the various faster payment rails (and traditional ones, too) can be time-consuming and costly.

Modern Treasury was founded to simplify, streamline, and upgrade payments operations across rails including RTP and FedNow. With APIs that automate money movement at scale and a web app for complete control over fund flows, Modern Treasury is the ultimate turnkey solution for faster payments.

We want to make sure your business is ready to take advantage of everything that FedNow can offer. Reach out to us to find out how we can help.

Get the latest articles, guides, and insights delivered to your inbox.